Scam prevention codes must save Australians from harm & trauma

Australia's scam crisis is a failure of systems, with Governments caught unaware as to how fast, complex and industrialised fraud crime is. This submission explains how organised crime exploits gaps in regulation, why current responses are making the problem worse, and what Government, Treasury and industry could do to stop the harm from financial crime ruining people’s lives.

Executive summary

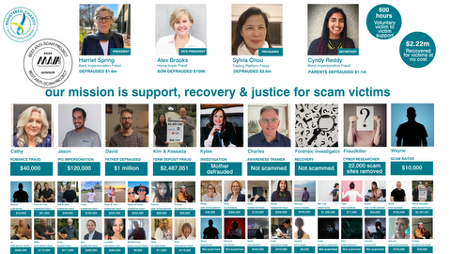

We are Australia's only self-funded, volunteer-led community, working directly to support victims through the complex harms global organised crime networks are wreaking on everyday citizens who trust their governments and banks to protect them.

We walk side-by-side with victim-survivors to deal with the overwhelming horror of financial crime, traumatic dispute resolution processes and broken enforcement systems in Australia.

Our ACNC-registered charity won the Best Anti-Scam Project of 2026 in the Money Awareness and Inclusion Awards. We helped consult with the United Nations Office on Drugs and Crime to develop the survivor-informed action brief to tackle fraud, which we implore the Government to implement.

We welcome the June 2026 Scam Prevention Framework (SPF) consultation, which rightfully shifts criminal responsibility onto corporations to prevent scams.

No country is untouched by the harm of scams, money laundering and illicit capital. Fraudsters, and corporate insiders typically scheme with other networked actors to specialise in finding the “legal loopholes” to commit deceptive fraud - please read Appendix H to understand the mechanics.

We stand by our January 2026 Scam Prevention Code submission, which included the following recommendations to protect Australians from the grave financial and psychological harm of scams:

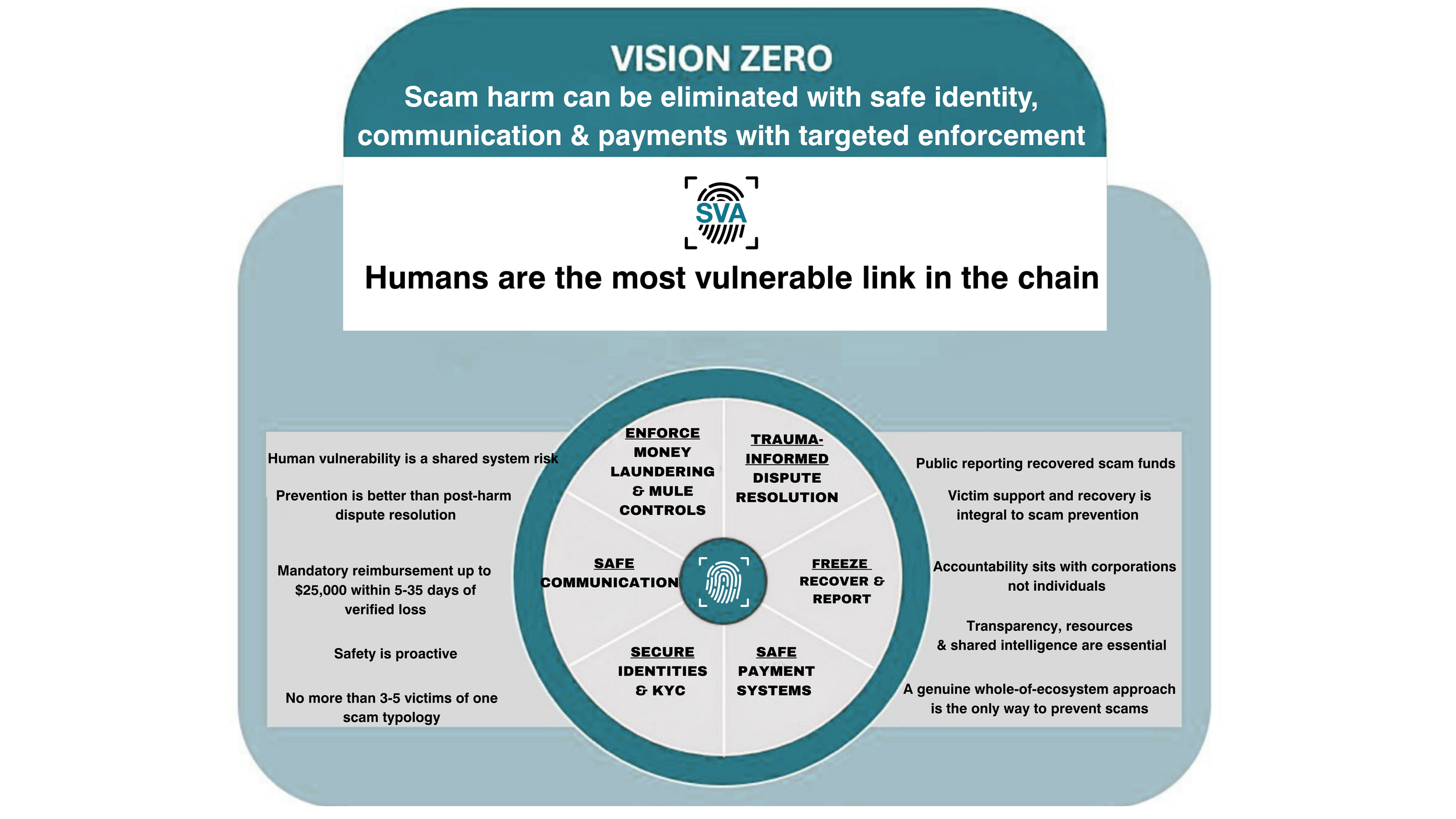

1. All entities in scam chains must be designated and follow prescribed fraud controls, with instant reimbursement up to $25,000 for re-used scam infrastructure.

2. Scam education improvement with a hotline and Scam Infrastructure League Table publishing clear Scamwatch reported warnings to centralise and harmonise the system.

3. Regulators and law enforcement must detect scam infrastructure using regulatory and law enforcement subpoenas, compiling anonymised data for publication and transparency. Actionable Scam Intelligence is urgent and must begin immediately.

4. Mandatory IDR reimbursement up to $25,000 for verified scam losses paid within 5-35 days.

5. All designated sectors must have clear reimbursement, freezing and takedown obligations backed by infringement powers for recovery and be fined within 30 days of a breach.

6. A Royal Commission into financial crime with 6-year common law protections to apply to receiving banks.

This new submission to the SPF Treasury consultation focuses on 3 chief concerns:

SECTION 1 Delays in making the SPF operational risks the regulations and codes becoming a “scam proliferation playbook”, where schemers will develop more sophisticated scams - specifically exploiting gaps in failing to designate online marketplaces. crypto ATMs and email scams

SECTION 2 More funding is needed for victim support through horrific Australian Financial Complaints Authority (AFCA) External Dispute Resolution (EDR) processes, particularly given the court orders made in the ASIC v HSBC case.

SECTION 3 A ‘safe systems’ approach is needed to solve the scam crisis, with transparent investigative resources dedicated to scam typologies replicated across more than 3-5 cases - high value scam syndicate activity must go beyond ‘investment’ and ‘romance’ typologies to truly protect Australians.

Our community are all volunteers following our ACNC charter to support victims at no cost to victims experiencing the highest harm.

SECTION ONE: The SPF risks becoming a scam proliferation formula as criminals exploit loopholes

AUSTRALIANS EXPECT GOVERNMENT TO PROTECT CITIZENS FROM CRIME, NOT EXPOSE THEM TO BLAME & VICTIMISATION

Scam and fraud victims get more support from the government and law enforcement after being punched and robbed on the street than they do losing hundreds of thousands of dollars to elaborate deceptions and fraud perpetrated through banks or online and telco communication channels.

We applaud the SPF’s attempts to tie ‘controls’ to reimbursement but it is simply unacceptable that the “whole ecosystem approach” will no longer cover the top contact method for scams - email. Crypto ATMs are increasingly used only for scamming and we believe an immediate ban on these is required. Banks are increasingly debanking mules to protect themselves as the SPF begins, but there is an urgent need for humane intervention of exploited and gaslit mules such as the woman outlined in Appendix B of this submission. The danger of job and romance scams morphing into harmful threat scams means online marketplaces must also be captured by designations to prevent harm.

We acknowledge the SPF’s mention of impersonation controls and urge the Treasury to specify this more clearly. We are seeing phone calls impersonating trusted authorities morphing into dangerous threat scams as criminal networks pretend to be from the Australian Federal Police, ASIC or the

“A BANK THAT OPENS AN ACCOUNT WHERE MONEY IS BEING TRANSFERRED BY A FRAUDSTER IS AN ACCOMPLICE TO FRAUD. IT IS NOT A QUESTION OF WHETHER OR NOT A BANK CAN RECOVER THE MONEY … IT IS A QUESTION OF WHETHER OF NOT A BANK IS PERMITTING A FRAUD TO TAKE PLACE BY NOT KNOWING WHO THEIR CUSTOMER REALLY IS.” - the former head of Royal Bank of Scotland Sir Peter Burt[5]

Australian Tax Office and coerce people into giving up valuable personal information and payments. One victim was under the control of the scammer for 21 days, sharing intimate details of her location - including when she was going to the toilet. Her bank, Westpac, now charges interest on her scammed loss of more than $840,000.

Close the AI Scam Gap: Consumer vulnerability should be anticipated as criminal networks weaponise AI agents, data theft and frontier AI models

The emergence of frontier models and AI agents creates new risks for Australians under the Scams Prevention Framework. As AI systems increasingly search, recommend and execute actions on behalf of consumers, scammers will manipulate those systems through false signals, coordinated disinformation and impersonation. Consumers are the weakest link in this chain of harm. The SPF should explicitly require banks to assess AI-mediated scam risks - particularly impersonation - and implement safeguards while committing to share intelligence across sectors. AI platform designations should be considered now as a matter of urgency, along with designating crypto, email and online marketplaces, where harm is already entrenched.

SECTION 1: Key recommendations:

A “whole of ecosystem” approach to the SPF is nonsense if email is not designated. The key information on email vectors that needs to be part of compliance statements include:

Device, location and personal data on who created the email account used in any part of a scam

The email header information behind emails misdirecting payments

Which platform - Gmail, Microsoft and Yahoo are commonly used - allowed the scam email to be sent

How the email breach likely occurred (this is currently very difficult due to multiple vectors of breaches and insider threats)

If any other domain is behind the email, e.g. travel.io, then who registered the domain

A signed compliance statement from the financial firm, other professionals (e.g. lawyers) stating there were no data breaches or insider threats.

Online marketplaces have high harm from scam syndicate activity tricking people into complex payment scams or using their online searches as ‘lead’ vectors to target people for other threat, job or relationship frauds. The type of information that needs to be on compliance statements from these frauds includes:

Who created the social profile - the email and mobile number and location data associated with it

The external URL links used to trick or deceive a consumer

The bank/payment account tied to any payment offers or advertising accounts

Crypto ATMs need to be banned, given their proliferation in Australia. Victims using these machines deserve to be counselled through humane interventions that help them understand how muling works. These gaslit mules pose a difficult challenge that will require corporations debanking them to resource appropriately and safely as part of the SPF.

SECTION TWO: Delays until 2027 expose Australians to more trauma, blame and theft

AFCA EDR PROCESSES TRAUMATISE VICTIMS - REFORM IS URGENT

The delays to hearing cases relating to the SPF until March 2027 are unacceptable.

The uncontested June 18 Federal Court case ASIC v HSBC demonstrated banks do not lack knowledge of their broken scam controls but will delay redress and force consumers to absorb the consequences. A bank’s highest legal obligation is to protect their shareholders, not uphold consumer laws.

Furthermore, the way AFCA amplified and escalated the harm upon HSBC victims seeking help from the ombudsman requires an urgent Government review. AFCA forced HSBC scam victims to sign “shut up and go away” goodwill payments which have now put victims in a complex position if they signed restrictive deeds to receive less than 100% reimbursement. Scam Victim Alliance calls on AFCA to reopen HSBC cases with the new evidence heard in the federal court and issue public determinations on each case for transparency.

AFCA created extensive delays for HSBC victims before its “Mr T” determination was passed 13 months after the victim’s initial scam. Even with the win of this determination, other HSBC victims whose scam operated in slightly different ways - which is common amonst all scam typologies - were shamed for “releasing more than one OTP” to their scammers and therefore denied justice and fairness.

HSBC’s pattern of denying scam liability and shifting the blame to other vectors has been replicated by other banks, including ANZ who also had SMS spoofing scams that resulted in severe losses to their customers. ANZ even allowed their customers to be robbed by mules on ANZ platforms, and AFCA’s determination still blamed the victim while claiming Australian law forces the ombudsman to make these determinations.

THE SCAM DOESN'T HAPPEN JUST ONCE. IT HAPPENS OVER AND OVER AGAIN. FIRST, MULES STEAL YOUR MONEY. THEN YOUR BANK OR SUPER FIRM TELLS YOU IT’S NOT THEIR RESPONSIBILITY. THEN YOU ARE PUSHED INTO A LONG, EXHAUSTING AFCA PROCESS THAT TAKES MONTHS OR EVEN YEARS. NO-ONE FULLY EXPLAINS HOW TO BEST ARGUE YOUR CASE.- Taylor, 43, scammed of $420,000 superannuation in a complex ASIC-registered managed investment collapse.

Scam Victim Alliance contends that AFCA has been misinterpreting the existing protections against fraud in Australian legislation because it doesn’t have case managers with the skill needed to pursue the full reaches of its fairness jurisdiction.

Furthermore, when AFCA seeks external counsel to get legal advice on complex situations like scams, many corporate legal firms are also incentivised to insist to AFCA that existing fraud protections under legislation and common law are unclear, as their firms make money from providing more complex advice. It is Scam Victim Alliance’s belief that existing laws protect against mules and money laundering, but the Government and regulatory timidity has prevented this happening.

AFCA’s dogged insistence that Australia required law reform before it could do better for scam victims is not strictly true. Our experience of supporting victims through the AFCA process is that the ombudsman service regularly:

Forces complainants to negotiate against themselves.

Fails to explain the legal concepts at play in the complaint until the very end of negotiations, when AFCA case workers commonly bully and intimidate complainants into accepting lowball offers “because that’s all they will get”.

Doesn’t demand corporations share required information for complainants (particularly with CCTV footage), refusing to identify whether AUSTRAC suspicious matter reports or systemic issues have been escalated as part of the case.

Victims must have overwhelming evidence of financial firm failures to win their scam case at AFCA. Read the raft of different victim experiences at AFCA on Product Review to see the reality of everyday citizens’ experiences with the financial ombudsman.

Resolves scam complaints that total up to $2.6 million over a range of transactions, but not a single scam loss involving $1.2 million in one transaction.

Refuses to use its ability to waive interest on scam losses, forcing victims to be exploited by their banks for profit in complex cases.

AFCA is increasingly claiming it doesn’t have “jurisdiction” so it can get out of having to deal with complex scam cases, with new complaints being ruled out before they go to case management (where there are lengthy delays).

Many of our victim community report their case managers refusing to embrace the complexity of their case. Victims from non-English speaking backgrounds not only cannot understand the process but can rarely find the words to challenge the case manager’s limited understanding. This is why information transparency is so important.

AFCA case managers betray the organisation’s own fairness jurisdiction by refusing to see connected scam typologies and treating them consistently. The following three cases all involved in-branch handling of email payment misdirection of property settlements, yet had extreme differences in AFCA determinations:

Mr and Mrs C Panel Determination- reimbursed 70%.

Mr F Panel Determination - reimbursed 70% but not the $1800 a month interest NAB charged on the scammed loss.

Mr & Mrs D Non-Panel Determination - reimbursed $0 and has now had to spend $110,000 taking civil legal action.

In cases (a) and (b), there was an extra connection with ‘hidden text’ in the payment instructions revealing a Commonwealth Bank customer was unwittingly or knowingly part of the networked scam infrastructure - the fact that AFCA treats each case in isolation rather than a systemic failure requiring complainant compensation demands urgent review. Not all AFCA cases reach determination, particularly if the bank agrees to settle - in these cases, like in Levin Salaberry’s homebuyer email fraud - the bank will reach a confidential settlement and force the complainant to sign a restrictive deed. AFCA endorses this approach.

It is up to the Australian Government to demonstrate stronger leadership than simply accepting AFCA’s poor interpretation of existing common law, legislative and code protections against fraud. Delays to the SPF have put citizens and taxpayers in harm’s way.

We know that regulatory reform is challenging, but the SPF was supposed to be in place by the first quarter of 2025. It is ludicrous that ‘industry consultation’ has forced more losses on consumers during the last two years. In the case where the regulator ASIC took rare action against HSBC after overwhelming evidence the bank forced hundreds of consumers to take the blame for broken systems.

We urge the Australian Government to re-examine the successful elements of the United Kingdom’s mandatory reimbursement scheme, which would have most high-harm cases reimbursed within 2 weeks of a financial crime upending their lives. This will not only prevent consumer harm but also cost the industry less over time, by keeping disputes out of AFCA.

POOR REIMBURSEMENT OUTCOMES AT AFCA PUT AUSTRALIANS IN HARM’S WAY

“WHEN I WAS SCAMMED IN 2012, I GOT ALL MY MONEY BACK. WHEN I WAS SCAMMED IN A JOB SCAM, I RECEIVED ONLY $6,000 NON-FINANCIAL COMPENSATION FROM AFCA. WHEN RECOVERY COMPANY PAYBACK CONTACTED ME, I PAID THEM BECAUSE I DID NOT REALISE IT WAS A SCAM. I COULD NOT BELIEVE HOW BADLY AFCA’S FAILED PROCESSES PUT ME AT RISK OF THESE PREDATORS.” - Vaishali, 42, lost $25,000 to a recruitment scam and $3500 to Payback.

Scam Victim Alliance ally, psychologist Caroline Micallef (see Appendix C) notes that individuals and the Australian taxpayer unwittingly bears the cost of scam harm, which doesn’t show up as a direct cost measured by Scamwatch statistics:

“In the last six years I have seen clients who are experiencing trauma from financial scamming. This is a new cohort of clients who, when they first discover they have been scammed, the psychological response is acute and overwhelming. Some immediate reactions can be physical illness, breathlessness, a sense their world has collapsed and can represent the onset of what often becomes a prolonged psychological crisis.

Not only have they lost money but sometimes the most important relationship in their life (romance scams, their savings, their creditworthiness, and sense of self worth. Victims often find themselves cut off from family and friends. The feeling of shame can be so pervasive it prevents victims seeking assistance and can persist for years after the financial loss.

The psychological effects extend well after the incident. There can be lasting anxiety and difficulty trusting others. Another response is grief, for loss of money, their savings, their credit rating and most of all, self worth. Without timely intervention, victims are likely to develop greater symptoms and difficulties that add to the burden on mental health services, homeless services, acute medical services and community welfare supports.

”

Fraud and scams are A national economic security problem

The highest harm scam victims are those facing losses greater than the current proposed mandatory reimbursement of $3,000. Victims with higher losses undeniably face more complex scam typologies (with 11-15 different networked elements exploiting loopholes). Many Australian victims are unwittingly placed at risk of recovery scams due to the complexity and barriers of AFCA’s limitations.

The complexity and holes in coverage of the SPF risks baking in the existing inequity and information asymmetry, which is causing untold personal, financial and mental anguish to Australian consumers.

Scam Victim Alliance Treasurer Sylvia Chou, who lost $2.6 million in a complex scam that started with a Facebook ad and ended with banks profiting from her misery, was sectioned in a mental health facility. The greatest mental distress came during dispute resolution at AFCA, when she expected an ombudsman to see the crimes that had been perpetrated against her. The threat of bankruptcy also meant she would not be able to earn an income as an accountant.

Most victims of high-loss scams face a long journey and legal battle, believing the initial scam is where the harm lies. It is only 3-6 months after their scam that victims realise they are in a constant state of anxiety and panic that is wearing them down mentally and emotionally. They hold out hope that AFCA’s dispute resolution can help them, only to realise very quickly that AFCA’s horrific processes blame and shame them for authorising their loss. We see this is the time when suicidal ideation and self-harm becomes a common experience in our victim community.

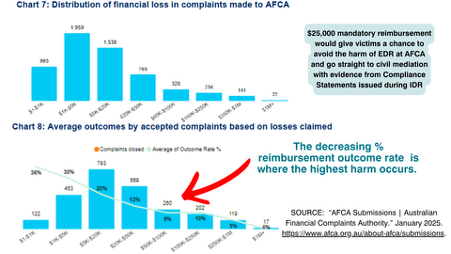

SOURCE: AFCA submission on the SPF in 2024

While the bulk of scam losses are at the lower end of the financial scale, mandatory reimbursement at $25,000 with full access to compliance statement evidence would protect victims from post-scam trauma harm.

Without considered pathways to de-escalate scams and fraud, Australia’s fragmented post-victimisation journey will continue to destroy savings, livelihoods and people’s trust in government and corporations.

If digital communication ecosystems continue being weaponised against citizens, this economic threat will quickly distort into a national security threat, too, where certain groups become radicalised forever.

“YOU JUST WANTED SOMEONE TO SAY SORRY FOR WHAT HAPPENED, BUT NOBODY DOES - THEY JUST BLAME YOU FOR AUTHORISING THE WHOLE STUPID THING.” - Frank, 72, a South Australian cancer survivor, lost $175,000 in a fraudulent property investment after moving his retirement savings due to concerns about “Trump’s war”. ASIC added the company to its Moneysmart Investor Alert List just four weeks after the scam

A mandatory reimbursement threshold of $25,000 will reduce costs for regulated entities over time by preventing thousands of low-value disputes from escalating into lengthy AFCA External Dispute Resolution (EDR) processes, which could cost multiple entities high determination fees.

We believe mandatory $25,000 reimbursement can help de-escalate the harm experienced by high-loss victims, as well as give them a starting point to decide whether to take their complex fight to civil courts and mediators, who may be better placed to deal with the situation.Mandatory reimbursement creates a stronger incentive for banks, telecommunications providers and digital platforms to invest in prevention, detection and disruption measures, as preventing scams becomes cheaper than managing disputes after harm occurs. It also reduces complaint volumes, administrative costs and reputational damage. A $25,000 threshold recognises that rapid intervention is more efficient than prolonged litigation-style processes. The UK experience shows that mandatory reimbursement is a stronger protective factor than having none at all.

Scam prevention should prioritise restoring consumers quickly and directing industry resources toward systemic risk reduction rather than costly post-harm disputes.

SECTION 2 SVA key recommendations:

Recognise the complex PTSD and harm scam victims in Australia face, and resource early intervention to stop the taxpayer bearing complex costs of scamming.

Reconsider delays to SPF and revisit the need to publish and share information with victims as part of a “safe systems” approach to resolving the scam crisis.

Harmonising and centralising scam prevention and investigation capabilities so victims can call one phone number to identify or report a scam (with language and translation for Mandarin, Arabic and Vietnamese language groups).

Ensure that mandatory reimbursement is re-examined to save greater costs and horrific delays by going through the AFCA process. We would be particularly keen to see a UK-style mandatory reimbursement scheme with a minimum $25,000 limit.

Understand that prompt and swift reimbursement avoids harm and will save Governments, corporations and taxpayers money over the long-term.

Consider funding complex AFCA cases with a “support fee” that corporations must pay in addition to other AFCA fees if case resolution takes more than 12 weeks at EDR.

SECTION THREE: Financial harm for high-loss victims is real and urgent

ASIC V HSBC HAS SET STANDARDS TO START OBLIGATIONS SOONER

The new consultation claims consumers are given IDR from 30 June 2026 and EDR from 1 January 2027, but there is no corresponding right for consumers to see or compare regulated entities' compliance performance before this time.

We contend the ASIC v HSBC Federal Court case demonstrates that some proposed SPF obligations may indeed have already moved beyond matters suitable for consultation.

We contend that the Federal Court case with HSBC may have created legal precedent necessary for stronger corporate controls to protect consumers. The Federal Court identified deficiencies in prevention, detection, investigation, remediation, governance and consumer restoration processes. The SPF should therefore distinguish between areas requiring innovation and those requiring mandatory baseline standards. “Reasonable steps” and principles-based flexibility cannot substitute for controls whose absence has already been judicially recognised as causing systemic consumer harm.

Comparing the Scam Prevention Framework with the Federal Court's findings in ASIC v HSBC

Flexible, principles-based obligations

Current SPF proposal

Flexible, principles-based obligations.

Federal Court finding

Some fraud controls are already objectively necessary.

Treasury could now examine

Introduce enforceable minimum standards before March 2027.

Scam intelligence sharing

Current SPF proposal

Better scam intelligence sharing, although Actionable Scam Intelligence is not yet clearly defined.

Federal Court finding

Financial institutions already possessed significant scam intelligence.

Treasury could now examine

Introduce mandatory reimbursement of up to $25,000 to create stronger incentives for industry prevention.

Industry capability

Current SPF proposal

Build industry capability over time.

Federal Court finding

Institutions had known about scam risks for years but failed to act transparently.

Treasury could now examine

Determine whether the real problem is a lack of intelligence—or a lack of enforcement.

Non-financial harm

Current SPF proposal

No recognition of non-financial harm.

Federal Court finding

The Court recognised non-financial harm in the Amended Joint Submissions on Liability and Relief:

"In the absence of those Key Controls, customers were at greater risk of suffering both financial loss and non-financial harm. Some customers did suffer those harms."

Treasury could now examine

Recognise human vulnerability as a system risk and introduce enforceable compensation for non-financial harm.

"Reasonable steps"

Current SPF proposal

Future-oriented regulation based on "reasonable steps".

Federal Court finding

Many minimum expectations have already been established by the Court.

Treasury could now examine

Create clear, transparent and enforceable obligations without requiring victims to pursue lengthy AFCA disputes.

Safe disruption powers

Current SPF proposal

Safe disruption powers.

Federal Court finding

Disruption itself can create consumer harm if poorly managed.

Treasury could now examine

Review and reform AFCA so dispute resolution no longer compounds victim harm.

The court’s orders to HSBC should now set the baseline for mandatory industry obligations, including AFCA’s oversight of previously determined cases. This is particularly important given the initial Government promises to roll out the SPF from the beginning of 2025. It is clear that delays have added to consumer harm and economic insecurity. HSBC victims are living, walking proof that this has occurred.

THE DISGUSTIFYING TRUTH OF BEING A SCAM VICTIM IN AUSTRALIA

One member of our community coined the word "disgustifying" to describe the moment she discovered the truth of how her bank, online social media and government failed to protect her. After draining her superannuation and making repeated payments through her bank to help her online partner "Alven" escape Syria, she learned that every dollar stolen had been funnelled through Australian banking money mules into what she now believes was accounts likely controlled by Africa’s ‘Yahoo Boys’ and scam networks. She had been tricked into taking out low-doc loans, which compounded her loss. The money she believed was saving the life of the online partner she had sent intimate photos to was instead helping fund what Interpol has described as a “global crisis” of human trafficking and other harms.

The SPF places significant obligation on industry but minimal new obligation on the Government to fund the investigative infrastructure required to pursue organised scam syndicates exploiting and weaponising Australian banking and communication infrastructure against citizens.

We believe there cannot be more delays in actionable scam intelligence and we need more regulatory capability to publish data around things like:

● Known mule bank accounts reported to Scamwatch, the Australian Financial Crimes Exchange, the Global Signal Exchange and state and federal law enforcement (this should be done regularly to help gauge how dangerous the banking system is for scams,

● Known spoofed telephone numbers used in previous frauds investigated by ASIC,

● Known accounts flagged to AUSTRAC through SMR and TTR reports that are associated with other known scam typologies.

We would also contend that part of the harm to victims is not adequately measuring scam losses or how effective warnings and education campaigns are. We would also ask the Federal Government to find a better way to measure the taxpayer impost of looking after scam victims after losing life-changing amounts of money.

Investment scams, superannuation fraud and the high-loss scams our victim community experiences do result in individual losses exceeding $100,000 and sometimes reaching more than $2,000,000. We have one particularly egregious case of a $6,000,000 scam.. These are more than opportunistic crimes - they involve scripted social engineering campaigns, professional money laundering networks and offshore coordination which evade the skill and capability of Australian regulators and law enforcement.

Home purchase fraud must also be recognised as a priority category. Property transactions in Australia routinely exceed $500,000 — in major metropolitan areas, frequently $1 million or more. Conveyancing scams, where criminals intercept communications between buyers, solicitors and conveyancers to redirect settlement funds, represent some of the largest single-victim losses in the scam ecosystem.

A first home buyer losing their deposit or settlement funds is not merely suffering financial harm. They are potentially losing decades of savings in a single transaction, with no prospect of recovery under the current framework and no realistic path to any meaningful redress.

These criminal attacks specifically target the conveyancing and legal sector, a largely unregulated scam surface under the current SPF. Email compromise at the point of settlement is a known, documented attack vector that has destroyed families financially and should be treated with the same investigative priority as superannuation fraud. Treating any of these crimes with the same resources allocated to a $500 parcel scam is problematic.

SECTION 3: SVA key recommendations:

SVA recommends the establishment of dedicated, properly resourced investigation units, with specific mandates covering:

● Large-loss investment fraud (individual losses exceeding $25,000);

● Superannuation scam syndicates;

● Home purchase and conveyancing fraud involving settlement fund diversion and laundering through gold, foreign currency and cash;

● Cryptocurrency-linked laundering networks connected to scam proceeds.

These investigation units should have direct access to AFCA complaint data, Report Cyber, ACCC Scamwatch reports and ASIC intelligence — with legal authority to act on cross-referenced leads without requiring victims to re-report through separate channels. It should report on recovered funds and make sure these are not put into general proceeds of crime pools, but dedicated to advancing protection and investigation of scams.

We would like to see Scamwatch offer a centralised service and co-ordinated phone line that gives victims realtime information on what is a known scam.

We believe a ‘safe systems’ approach is urgently needed - see Appendix E - How safe systems can help.

We believe Scamwatch needs to report the recovered scam money as well as scammed losses. Singapore now does this. Currently, Australian banks have no accountability to show those funds have truly disappeared and simply lie to AFCA and get away with it.

We know that JPC3 is working in cooperation with the AFCX and there have been successful intelligence sharing that now stops money leaving Australian shores - so why aren’t banks recovering more funds for scam victims? How can the Australian Government make the chain of custody more accountable to scam victims who simply cannot believe the lies they are told after they’ve fallen victim to criminals exploiting gaps in our systems.

Mandatory reimbursement leads to Scam Resilience: stronger together

The UK's 2026 Annual Fraud Report demonstrates why Australia's Scams Prevention Framework (SPF) must be built around systemic prevention and fund recovery with mandatory reimbursement rather than a slow and steady approach to ‘reasonable steps’.

Fraud is both an industrialised crime and a national security threat. In 2025, the UK recorded a record 4.06 million fraud cases, an 11 per cent increase on the previous year, with £1.28 billion stolen from consumers and businesses. On average, eight UK people were defrauded every minute and almost £2,500 was stolen every minute. Yet banks simultaneously prevented £1.68 billion in unauthorised fraud, stopping 70 pence of every £1 of attempted theft. In Australia, our banks will brag about their investment in anti-fraud measures while simultaneously blaming victims for authorising transactions into mule accounts hosted on their platforms.

The latest UK information shows the fastest growing scams are no longer traditional bank impersonation scams. Losses from investment scams reached a record £221.5 million, purchase scams £118.1 million, romance scams £39.2 million and advance fee scams £58.4 million. These scams overwhelmingly originate online, with 66 per cent of APP fraud beginning on digital platforms and a further 17 per cent via telecommunications channels.

The rise of elaborate deceptions around the globe demonstrates that criminals are increasingly exploiting artificial intelligence, impersonation, deep fakes, threats and social engineering rather than technical vulnerabilities. The SPF should therefore recognise that victims are not failing because they lack intelligence or awareness. Criminals are exploiting predictable human behaviours at industrial scale. Australia's response must move beyond consumer education towards enforceable, shared obligations across banks, telecommunications providers, digital platforms, dating applications, crypto platforms and emerging AI agents and a holistic supportive scam recovery pathway. We need law reform across the board to deal with fast-changing crime vectors.

ENDNOTES

1. “INTERPOL Report Warns of Increasingly Sophisticated Global Financial Fraud Threat.” Accessed June 20, 2026. https://www.interpol.int/News-and-Events/News/2026/INTERPOL-report-warns-of-increasingly-sophisticated-global-financial-fraud-threat.

2. “Scam Victim Alliance Winners 2026.” The MAIAs - Money Awareness & Inclusion Awards, n.d. Accessed June 19, 2026. https://www.maiawards.org/winners-2026/.

3. United Nations Office on Drugs and Crime. (2025). Survivor-informed action brief on combating fraud. United Nations. https://www.unodc.org/res/organized-crime/GFS/publications/UNODC_Survivor-informed_action_brief_on_combating_fraud.pdf

4. Scam Victim Alliance. “Scam Victim Alliance Urges 6 Changes to SPF Designations and Codes to Protect Australians.” Accessed June 21, 2026. https://scamvictimalliance.org.au/submissions-blog-updates/cash-mandate-submission-sva-d94mh.

5. “Cryptocurrency ATM Scams | AUSTRAC.” Accessed June 20, 2026. https://www.austrac.gov.au/general-public/cryptocurrency-atm-scams.

6. 7NEWS. “The Single Email That Cost an Australian Woman $732,000.” May 4, 2022. https://7news.com.au/business/property/wa-woman-loses-732000-to-property-scam-after-responding-to-fake-email-c-6674754.

7. Commonwealth of Australia Federal Court of. “ASIC v HSBC Bank Australia Limited.” Text. Federal Court of Australia, June 19, 2026. https://www.fedcourt.gov.au/services/access-to-files-and-transcripts/online-files/asic-v-hsbc.

8. Hussain, Ali. Pay out to Fraud Victims, Demands Ex Bank Chief. n.d. Accessed June 21, 2026. https://www.thetimes.com/business/companies-markets/article/pay-out-to-fraud-victims-demands-ex-bank-chief-qskv2rc55vv.

9. Scamwatch. “Scam Statistics.” Text. Australian Competition and Consumer Commission, April 8, 2026. Australia. https://www.scamwatch.gov.au/research-and-resources/scam-statistics.

10. “Determination For Case 12-00-1016692 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=f9f8941f-7379-ef11-ac20-000d3a6acbb4.

11. “Determination For Case 12-24-130239 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=ba8cf7fe-c58e-f011-b4cc-00224892c723.

12. “How AFCA Makes Decisions | Australian Financial Complaints Authority.” Accessed June 22, 2026. https://www.afca.org.au/what-to-expect/how-we-make-decisions.

13. ProductReview.Com.Au. “Australian Financial Complaints Authority (AFCA) Reviews.” June 14, 2026. https://www.productreview.com.au/listings/australian-financial-complaints-authority-afca.

14. “Determination For Case 12-00-1045764 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=add1b211-8384-f011-b4cc-002248112dcc.

15. “Determination For Case 12-00-1061026 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=8894dc11-27c4-f011-bbd3-7ced8da1919d.

16. “Determination For Case 12-00-1034883 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=548b5513-5825-f011-8c4d-002248937998.

17. Content Renegade - Alex Brooks. Alex Brooks Asked MP Stephen Jones Financial Services Minister about Scams. 2024. 04:56. https://www.youtube.com/watch?v=2HZ9P36wg-A.

18. “One Year on: Impact of APP Reimbursement on Victims.” Accessed June 20, 2026. https://www.psr.org.uk/news-and-updates/latest-news/news/one-year-on-impact-of-app-reimbursement-on-victims/.

19. “Alert: Money Recovery Scam Using Fake Documents to Impersonate ASIC – Www.Payback-Recovery.Com.” News item. Accessed June 22, 2026. https://www.asic.gov.au/about-asic/news-centre/news-items/alert-money-recovery-scam-using-fake-documents-to-impersonate-asic-www-payback-recovery-com/

20. “Investor Alert List - Moneysmart.Gov.Au.” Accessed June 21, 2026. https://moneysmart.gov.au/check-and-report-scams/investor-alert-list#!impersonation-of-oakmere-capital-pty-ltd-oakmere-capital-com--4258

21. Australia, Commonwealth of Australia Federal Court of. “ASIC v HSBC Bank Australia Limited.” Text. Federal Court of Australia, June 19, 2026. https://www.fedcourt.gov.au/services/access-to-files-and-transcripts/online-files/asic-v-hsbc.

22. Duffin, Perry. “The Nigerian ‘Blood Cult’ Targeting Lonely Australians with Romance Scams.” Stuff, April 4, 2025. https://www.stuff.co.nz/world-news/360641133/nigerian-blood-cult-targeting-lonely-australians-romance-scams.

23. INTERPOL releases new information on globalization scam centres. Available at: https://www.interpol.int/en/News-and-Events/News/2025/INTERPOL-releases-new-information-on-globalization-of-scam-centres (Accessed: December 30, 2025).

24. UK Finance. “Annual Fraud Report 2026.” Accessed June 16, 2026. https://www.ukfinance.org.uk/policy-and-guidance/reports-and-publications/annual-fraud-report-2026.

25. “Are Technical Support Scams Getting More Advanced?” Accessed June 21, 2026. https://blog.gaborszathmari.me/are-technical-support-scams-getting-more-advanced/.

26. Scam Victim Alliance. “Deceived! An Investment Scam Nightmare for Sylvia Chou.” Accessed June 25, 2026. https://scamvictimalliance.org.au/victim-survivor-stories/scammed-silenced-and-still-fighting-sylvias-26m-battle-for-justice.

27. “Investor Alert List - Moneysmart.Gov.Au.” Accessed June 25, 2026. https://moneysmart.gov.au/check-and-report-scams/investor-alert-list#!gg-capital-group-limited-trading-as-bluelexus--1236 .