industrialised lead generation IS a financial crime blind spot

Superannuation fraud is no longer primarily a consumer protection problem. It is a national economic security problem. The First Guardian, Shield and Australian Fidiciaries Ltd collapse of ASIC-registered managed investment schemes needs transparency and reforms to prevent more Australians losing their superannuation.

Executive summary

Scam Victim Alliance is a community of fraud victims supporting hundreds of Australians through the trauma that follows life-changing financial crime.

We welcome Treasury's recognition that lead generation sits at the beginning of the chain of events that can ultimately cause significant consumer harm.

Our experience suggests the problem may be larger than currently recognised, with “check your super” advertising thriving online.

Lead generation has evolved into the industrial front-end of organised financial crime and fraud. Today's criminal enterprises use the same advertising technology, behavioural profiling and customer acquisition techniques as legitimate businesses. Australians searching online to compare their superannuation, invest for retirement, recover scam losses or simply look for a new job can unknowingly enter sophisticated fraud funnels designed to identify, influence and eventually exploit them.

A compromised online banking login can reportedly be purchased for less than US$10. Digital advertising can then be used to identify and recruit thousands of potential victims at scale. Artificial intelligence is accelerating this process, making scams cheaper to run, more convincing and far harder to detect.

Australia's regulatory framework has not kept pace.

Our submission argues that lead generation should be viewed as critical financial fraud infrastructure rather than simply another form of advertising.

Unless governments regulate the beginning of the fraud journey, enforcement will continue to occur only after Australians have already lost their homes, retirement savings and financial security.

7 key Scam Victim Alliance recommendations to improve lead generation

Assume all Australians are targets for organised cybercrime as low-cost cybercrime-as-a-service offers shifts profit incentives towards criminal extraction of wealth from Australia’s legitimate banking and superannuation systems.

TAKEAWAY: Recognise fraud as an economic productivity and national security threat and respond quickly as AI and Quantum computing rapidly amplify the harm.

Ban algorithmic digital advertisingfor high-risk financial products, including scam recovery, comparing superannuation, investing, AI trading, creating SMSFs and “investing in property through your super”. Mandate that digital platforms, registered businesses and AI platforms retain advertising viewed against on user profiles to ensure victim redress and a successful ‘whole of system’ approach to preventing, disrupting and enforcing scams and fraud.

TAKEAWAY: Build technical capture and licensing requirements into lead generation and fraud facilitation - including ‘native content’ and ‘educational content’ and ‘website quizzes’ to ensure fraud victims can trace back the social engineering pathways after they have suffered a loss. It is critical that platforms capture and save financial services ads to be able to trace back which actors placed and profited from the lead generation and the downstream commissions.

Ban high-harm vehicles and facilitators for fraud such as weak auditors and crypto ATMs The best fraudulent schemes lay the groundwork over months, much like the First Guardian-Shield lead generation systems. Preventing the manipulation of Australians into believing a scheme is in their best financial interest is where the focus should be. Prohibiting social engineering through misleading online articles, website tools to “compare super”, “recover scam losses” or invest in “AI trading” used as lead capture unless independently verified and transparent with clear license numbers, with domain registrants also required to keep data on corporate entities..

TAKEAWAY: Introduce civil and criminal liability for professional facilitators — including lawyers, accountants, auditors, company formation agents, crypto ATMs, SMSF creators — who recklessly enable the creation and scaling of fraudulent financial schemes.

Adopt a victim-centred and ‘safe systems’ approach to fraud redress, including law enforcement follow-up, mandatory reimbursement and no-cost victim support through the Australian Financial Complaints Authority, as per Australia’s pledge at the UN Global Fraud Summit[1].

TAKEAWAY: Establish a national fraud strategy, similar to Britain’s Fraud Strategy 2026-2029[2] policy paper to guide a cohesive regulatory and enforcement approach

Ensure government identities cannot be forged to create more mule accounts which continue fraud harms. The Treasury must recognise the growing economic absurdity of identity fraud: leaked driver licence and passport credentials can be purchased online for under $10, while governments and victims bear replacement and remediation costs many times higher — often $30 or more for a driver licence and substantially more for passports and associated recovery processes.

TAKEAWAY: Australia should examine integrated anti-fraud identity models such as Singapore’s Singpass and MyInfo framework, which securely connects government identity verification with banks, telecommunications providers and regulated institutions in real time. A nationally coordinated digital identity ecosystem would significantly reduce impersonation fraud, mule account creation and document misuse while lowering long-term remediation costs for both governments and consumers.

Make fund recovery of fraud reportable and measurable. Singapore is already capturing this data[3] to measure how much of its citizen legitimate wealth is being hijacked by cybercrime to fund and scale further global crime harms.

TAKEAWAY: ACCC’s Scamwatch should report fund recoveries, not just reported scam losses. Australia should make fraud recovery rates formally reportable and measurable across banks, regulators and law enforcement agencies, recognising that stolen money is not simply an individual consumer loss but part of a global criminal economy that funds wider harms including human trafficking, child exploitation, drug trafficking and wildlife crime.

Hold a royal commission into financial crime and fraud. Australia should establish a Royal Commission into financial crime and fraud to examine the rapid industrialisation of scams, superannuation investment fraud, mortgage fraud, cyber-enabled theft and organised money laundering across the economy.

TAKEAWAY: Financial crime is no longer an isolated consumer issue — it is a growing national economic security threat. A Royal Commission would help expose the scale of organised fraud operating across Australia, identify systemic failures and build the coordinated safeguards, intelligence-sharing systems and accountability mechanisms needed to protect Australians from increasingly sophisticated transnational criminal networks, as Australia pledged at the recent UN Global Fraud Summit.

All Australians with money are ‘leads’ for malicious fraud schemes

Lead generation, cold-calling and other forms of ‘marketing’ create predictable pathways for fraud that begin long before any money is lost. Even before AI accelerated the disruption of financial services markets, consumers have long relied on Google searches, online ads, comparison tools and word of mouth advice from friends, as well as aggregators like Product Review or TrustPilot.

In a modern digital economy, individuals have their details and online cookies captured and passed along simply by reading legitimate commercial news websites. Scammers increasingly recruit victims through the same algorithmic advertising infrastructure that underpins Australia’s commercial news ecosystem.

Diagram (ii) Algorithmic ads on TheAge.com.au recruit leads for a range of businesses, both legitimate and illegitimate

Major publishers rely on a layered ad-tech stack—including content recommendation engines such as Outbrain and Taboola, programmatic ad exchanges like Google Ad Manager and supply-side platforms such as Magnite—which dynamically auction and optimise content placement based on engagement metrics. These algorithmic systems are designed to maximise click-through rates and user attention, not to assess the legitimacy of underlying content. As a result, scam actors can cheaply purchase targeted exposure and exploit behavioural profiling tools, which sell cheaply to the types of actors who orchestrated the First Guardian and Shield collapse.

Note that a ‘high value individual’ can be someone who is looking at content relevant to a major life event like trying to find a new job, getting married, having a baby, moving house, planning retirement or looking to invest. All of these life events are ‘leads’ for malicious industrialised fraud actors who have breached Australia’s trusted infrastructure (such as the Penthouse Syndicate inside NAB).

This creates an environment where fraudulent investment ads, impersonation content, and other scam vectors are distributed at scale alongside legitimate journalism. The fragmentation of responsibility across multiple intermediaries further weakens accountability, enabling scammers to rapidly test, iterate, and optimise deceptive campaigns in ways that mirror legitimate digital marketing practice, where algorithmic advertising ramps up the harms.

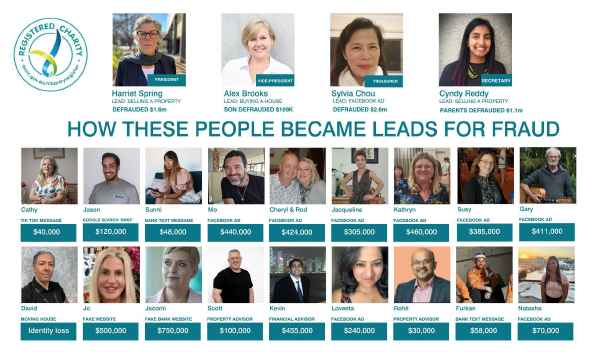

Evidence from the First Guardian and Shield collapse Facebook and Google ads highlights how industrialised and algorithmic lead-generation ecosystems create the on-ramp for large-scale financial harm. Testimony indicates the existence of organised “lead gen” networks in Queensland and Victoria spruiking website landing pages that got people to ‘check their super’ or ‘compare their super’. Actors from these schemes have told Scam Victim Alliance that between $20m and $40m was spent on digital ads over several years recruiting the 10,000 to 12,000 people who later lost money to these schemes.

The First Guardian and Shield loss experience further suggests that regulators can only detect misconduct after funds have been misappropriated. The collapse of Australian Fiduciaries Ltd followed a similar pattern, with nurses particularly exposed to the ‘lead-engage-convert’ model spruiking collapsed NDIS property schemes that enriched multiple .

The challenges experienced by consumers seeking redress through mechanisms such as the Australian Financial Complaints Authority, the Compensation Scheme of Last Resort, the CDDA or Act of Grace discretionary schemes highlight a deeper structural issue that requires urgent resolution.

There is a massive accountability gap for regulators, government agencies and trusted corporations holding credit, investment and other financial services licences while redress for harm remains limited and fragmented. When harm arises from lead generation practices that fall into regulatory grey areas, agencies and corporations will never be seen to have breached a specific duty.

When consumers can suffer significant financial loss without access to meaningful redress, it means our regulatory and enforcement frameworks do not adequately capture the early-stage conduct that set the harm in motion. This misalignment between how harm actually occurs and how responsibility is assessed underscores the need to bring lead generation activities more clearly within the regulatory and enforcement perimeter.

Strengthening oversight of lead generation is therefore not only a preventative measure, but a necessary step to restore accountability across the system. By clearly defining when lead generation activities constitute a financial service, extending obligations to those who influence consumer decision-making, and addressing incentive structures that prioritise conversion over suitability, the regulatory framework can better reflect the realities of how financial harm occurs. Without these reforms, compensation schemes will continue to struggle to deliver outcomes for affected consumers, as the origin of harm remains structurally disconnected from the points at which responsibility is currently assessed.

Artificial Intelligence is scaling harm

Artificial intelligence is improving efficiency across the financial system, but also amplifying risks like synthetic identity, misinformation, disinformation and fraud. Our community has lived experience (and large financial losses) which show structural apathy, political inertia, and financial institutional design failures are scaling the financial harm.

Consumers are often presented with promotional content that mimics trusted guidance, without clear, consistent or comparable disclosure of commercial intent, remuneration structures, or the risks associated with the recommended actions. By the time an unwitting consumer is on a call with an adviser or lead generator, they are already primed to accept bad advice.

Digital platforms have enabled the large-scale use of low-cost, algorithmically targeted advertising to circumvent longstanding protections such as bans on cold calling. Our engagement with victims involved in recent collapses such as First Guardian, Shield, Australian Fiduciaries Limited and Lion Property indicates that this ecosystem remains active. Advertisements across platforms such as YouTube and Facebook continue to funnel consumers into conversations with entities functioning as lead generators, operating under business models driven by switching fees and downstream commissions. These interactions frequently lead consumers toward complex and high-risk strategies—including SMSFs, leveraged property investment, scam recovery or speculative offerings—without the benefit of clear, standardised, and consumer-tested disclosures that would enable genuine comparison or informed consent.

Meanwhile, the corporations at the heart of these schemes also seem able to set up property developments and managed investments that also defraud banks and other finance companies by double-mortgaging assets that have little to no regulatory scrutiny. This submission calls for urgent reform: banning algorithmic ads for high-risk products, mandating licensing and vetting of all promoters, prohibiting deceptive comparison platforms, and adopting victim-centred enforcement including restitution and protections from further penalties.

OXIL research shows scam and fraud targeting is now based on situational vulnerability

Large-scale analysis of scam activity shows that modern fraud is not random but engineered. Lead generators build trust through a ‘funnel’ that starts with a signal of intent from a vulnerable consumer. Digital platforms succeed at not simply marketing, but also scaling systems in which individuals are identified, filtered and engaged at moments when they are most susceptible to influence.

By leveraging personal and behavioural data, lead generation systems are able to prioritise those most likely to respond, effectively targeting vulnerability at scale. These systems operate using a combination of broad exposure and targeted engagement. Consumers may first encounter generalised advertising, but are quickly funnelled into more personalised interactions that build trust and momentum over time. This creates industrial-scale pipelines of potential victims, where influence is applied progressively rather than at a single point of decision. By the time a financial product or investment opportunity is presented, the individual has often already been psychologically primed, making the eventual decision appear voluntary while being shaped by earlier interactions.

When engagement, phone calls and relationship building is driven by repeated exposure, emotional cues and tailored messaging, traditional notions of consent—such as clicking on an advertisement or opting in to be contacted—do not reflect genuine understanding or agency.

This means the Treasury must urgently support a shift in regulatory approach. Rather than placing responsibility primarily on individuals to identify and avoid harm, there is a clear need to recognise lead generation as part of the broader harm pathway. This requires a safeguarding model that addresses risks earlier in the chain, ensuring that systems capable of identifying and influencing vulnerable consumers are subject to appropriate oversight, accountability and intervention.

Fraudsters have been emboldened by Australia’s weak approach to enforcing the law or addressing cyber-enabled financial harm. Fraudsters can use technology, fake identities, social media and sophisticated financial schemes to steal billions from ordinary Australians every year. These crimes hurt families, destroy retirement savings and weaken trust in banks, government and the financial system itself.

Scam Victim Alliance contends that improving identity protections, stopping dangerous advertising practices, holding facilitators accountable and building stronger cooperation between banks, regulators and law enforcement, Australia can make it much harder for organised fraud networks to operate. We believe money laundering laws can be used more effectively to stop the harm.

Fraud prevention should not depend on ordinary people spotting highly sophisticated crime on their own. Australia needs safer systems, faster action and stronger accountability before more people lose their homes, savings and futures.

Endnotes & references

Scam Victim Alliance. About Scam Victim Alliance.https://scamvictimalliance.org.au/about

Voce A, Morgan A. The Costs of Serious and Organised Crime in Australia. Australian Institute of Criminology, 2025.

Reserve Bank of Australia. Financial Stability Review: Financial Stability Implications of Artificial Intelligence. September 2024.

United Nations Office on Drugs and Crime. Global Fraud Summit 2026 Pledges.

UK Government. Fraud Strategy 2026–2029.

Ministry of Home Affairs (Singapore). Scam Loss Recoveries in the First Half of 2025.

Dastoor C. Calls to Fix Shield, First Guardian Anti-Hawking Loophole. Professional Planner, 20 August 2025.

Taylor C, Taylor A, Sutherland J, Hakmeh J, et al. Rethinking Scam Prevention: Large-Scale, AI-Powered Analysis for a Safeguarding Approach. Oxford Information Labs.

Taylor, Carolina Caeiro, Alice Taylor, James Sutherland, Joyce Hakmeh, Emily. “Rethinking Scam Prevention: Large-Scale, AI-Powered Analysis for a Safeguarding Approach - Research.” Oxford Information Labs. Accessed April 20, 2026. https://www.oxil.co.uk//research/rethinking-scam-prevention-large-scale-ai-powered-analysis-for-a-safeguarding-approach.