Kevin paid $455,000 to buy a house from Lion Property Group - what he did next might surprise you

When Kevin bought a new townhouse to live in, he invested $455,000 into a Lion Property Group development with contracts securing the funds in trust. Instead, Lion group collapsed in a $122.5 million black hole of intermingled investor funds and related-party transfers affecting 600 Australians. You’ll never guess what Kevin did next.

When Kevin moved from Hong Kong to Melbourne, he thought his new home would be part of a boutique property development

Most people characterise investment fraud victims as chasing investment returns that are “too good to be true”

But Kevin Shari did his due diligence.

He was working in Hong Kong and wanted to buy a house in Melbourne to move to Australia.

A connection in Hong Kong suggested Kevin meet with a Lion Property Group sales director named Michael Peroumal who promised that Kevin could buy a brand new townhouse in the company’s Noble Park development, paying $455,000 including amounts associated with 455 units in the Parkside Noble Park development for his new home.

Kevin paid $455,000 to buy a townhouse in this development. He claims to have been threatened with violence.

Lion Property Group directors claimed to have spent time working in Australian banks

Kevin was issued a contract of sale for his new townhouse and in 2020, when COVID-19 struck and caused building delays in Melbourne, Lion Property Group paid Kevin $1300 or so each month to cover his rent.

It seemed reasonable. It seemed legit.

Lion Property Group brochures claimed “Our Property Development investment model allows us to create wealth, build homes, and change lives.”

In 2023, Lion Property Group’s monthly payouts to cover his rent suddenly stopped. Other Lion Property Group investors took court action.

The nearly 600 mum and dad investors had all been sold a different story as to why they should invest in Lion Property Group - including Loveeta D’Souza’s family, who invested $30,000. Most investors were convinced by friends or by the Facebook and Instagram ads that Lion’s unique approach to ‘boutique property development’ would offer decent returns.

After court, KPMG liquidators were brought in to take control of the company, investigate where the money went, sell the boutique developments, and try to recover as much money as possible for the investors and people owed money before shutting the business down

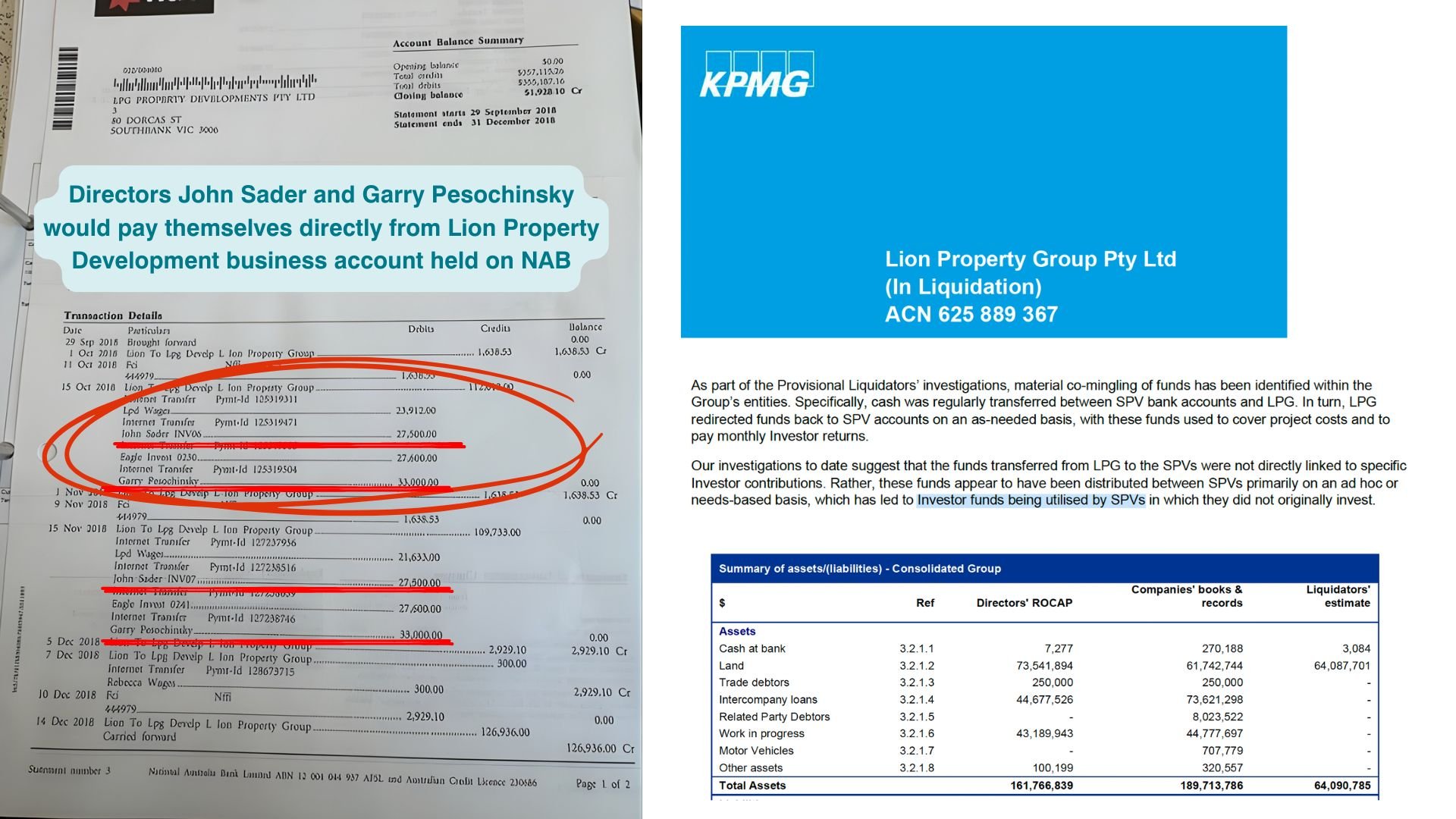

KPMG’s first report was shocking, with Australian Property Investor reporting that the company directors had moved $25 million of investor funds into other companies that benefited the directors in what looked like a Ponzi-style scheme, where new investors were paying earlier investors their monthly ‘returns’.

Although the Supreme Court refused Kevin leave to continue separate litigation against Syndicate 13 while in liquidation, the decision recognised that his allegations raised serious questions and directed the dispute into the liquidation process.

But Kevin simply wanted the house he had bought. He began to teach himself how to represent himself at court.

Kevin Shari has represented himself in court and found evidence of company directors paying themselves $27,000 and $33,000 a month in wages.

The liquidators found Lion Property Group had more than 20 NAB business accounts containing just $3000 when the group went bust.

As seen in the collapses of Shield Master Fund and First Guardian, the company directors — John Sader and Garry Pesochinsky, who benefited during the fundraising phase — later argued that the liquidation worsened the company’s financial troubles and accelerated its collapse.

Lion Property Group used different “special purpose vehicles” to raise millions from investors between 2018 and 2024, with Facebook and Instagram ads promising Lion’s special approach would return the investors’ capital once boutique property projects were completed and sold.

Lion Property directors denied allegations in court that they operated as a Ponzi-style scheme, blaming Covid-related construction delays, rising interest rates, and legal disputes for the collapse. They argued that delayed townhouse developments in Camberwell severely damaged the company’s cash flow.

Despite these claims, investors faced devastating losses, with many expected to recover only a small fraction of their money. The Lion Property developments are being sold through mortgagee fire sales, while secured debts and multiple mortgages over the property developments have significantly reduced the remaining value available to investors.

Kevin has taken legal action against lawyers and banks associated with the Lion Property Group collapse but his newest move will see the Victorian Chief Commissioner of Police on trial in the Supreme Court in June 2026.

“The best I can do is get the police to do a risk assessment based on violent threats against me by the directors involved in the Lion Property collapse,” Kevin said.

“What I am asking for is not special treatment. I am asking police to assess the risk properly, because there were threats, serious financial loss, and an ongoing collapse affecting hundreds of Australians.”

Kevin realises how little chance he stands in any of his legal actions, as fraudsters are emboldened by Australia’s weak controls.

Once ASIC - the corporate regulator - begins investigating, people like Kevin are held hostage to liquidators painstakingly following where the money has ended up in complex schemes that transfer money between different corporate entities.

Kevin’s story also exposes a deeper problem: Australian law treats ‘investment fraud’ ‘as an individual consumer mistake rather than an economic crime problem.