AFCA must Reopen HSBC Scam Cases Following Historic Federal Court Findings

The Federal Court's landmark $35 million fine and findings against HSBC cast doubt on whether scam victims received fair outcomes through AFCA. Scam Victim Alliance is calling for affected cases to be reopened so victims can receive the full compensation they should have received in the first place.

The Federal Court's findings and $35m fine against HSBC raise broader questions about whether Australia's external dispute resolution system can deliver timely and fair support and compensation for scam victims whose losses resulted from systemic failures in Australia's banking system. Scam Victim Alliance is calling on AFCA to oversee affected cases and ensure that the under-compensation and victim-blaming .

Scam Victim Alliance (SVA) is calling for all HSBC scam victim cases that were denied, under-compensated, or settled through AFCA’s traumatic dispute resolution processes to be urgently reopened following the Federal Court's landmark findings against HSBC Bank Australia.

On 18 June 2026, the Federal Court ordered HSBC to pay $35 million in penalties after finding widespread failures in fraud prevention, customer investigations and account restoration processes.

The Court found that HSBC failed to have adequate systems to prevent and detect unauthorised transactions, failed to comply with ePayments Code requirements in 97% of cases, and failed to properly advise customers how to regain access to their accounts after restrictions were imposed.

Scam Victim Alliance believes these findings fundamentally call into question the fairness of previous AFCA outcomes and published determinations for many victims who sought redress through the Australian Financial Complaints Authority (AFCA).

Many victims endured lengthy and traumatic complaint processes while attempting to recover money lost through criminal mule and money laundering activity.

SVA has serious concerns that some victims felt pressured by AFCA to accept low settlement offers and confidentiality agreements simply to obtain partial reimbursement when they were desperate to reclaim their life savings.

The Federal Court findings raise questions about the barriers Australian scam victims face, particularly being forced to be told their losses were their own responsibility when the Court has now established that HSBC's failures were widespread and systemic.

Scam Victim Alliance is calling for:

All HSBC scam victims who did not receive 100% reimbursement or interest on their losses to be reopened and compensated through AFCA;

A moratorium on relying upon previous AFCA determinations and/or deeds for “full and final settlement” involving HSBC scam complaints;

A regulatory review of AFCA’s harmful and traumatic dispute resolution processes for scam victims, already in shock and financial distress after being victims of crime and systemic weaknesses in our banking system;

A review of failed detection of systemic issues when similar scam typologies involving criminal exploitation of Australian financial payments systems go unreimbursed;

The publication of all data showing how many HSBC spoofing and scam victims accepted confidential settlements and the shortfall of each settlement compared to the loss;

An independent examination of whether AFCA processes compounded victim harm with a view to working towards how AFCA can move towards a trauma-informed external dispute resolution process in line with the United Nations Office on Drugs and Crime survivor-informed action brief on combatting fraud.

AFCA to examine making each HSBC victim truly financial ‘whole’ after the court findings, including non-financial compensation and lost interest; Immediate reforms to AFCA’s scam dispute resolution processes to ensure victims are not forced through prolonged and re-traumatising dispute resolution processes given the ongoing delays in the Scam Prevention Framework rollout.

The Court accepted that HSBC had known for years that fraud risks against its customers were increasing, that there had been a lack of investment in fraud controls, and that additional controls were available to better protect customers.

It also recognised that customers suffered both financial and non-financial harm.

Scam Victim Alliance says this case exposes a broader national problem.

“Scam victims are harmed three times: first by organised criminals, then by corporate and institutional failures, and finally by exhausting civil dispute resolution processes at AFCA or in the civil legal system that force them to repeatedly relive their trauma,” said Scam Victim Alliance president Harriet Spring.

"The HSBC case exposes a disturbing truth: institutions can know where the risks are within their own systems, yet still force consumers to absorb the harm. It simply has to stop. All people victimised by criminal scams deserve the corporations who failed them to compensate,” she said.

“Australian scam victims denied fair outcomes at AFCA deserve another chance after these court orders. Justice must extend to every victim left behind by AFCA and Australia’s poor justice process for those fleeced by criminal scammers."

Consumers should not bear the cost of delayed investments in fraud detection while money mules and money laundering proliferates in our banking system.

As Assistant Treasurer Dr Daniel Mulino proposes delaying implementation of the Scams Prevention Framework beyond its initial start date of 2025, stronger scam protections cannot wait until 2027.

Every delay creates more victims and exposes more Australians to criminals fleecing them while corporations and AFCA push the blame and cost on to consumers.

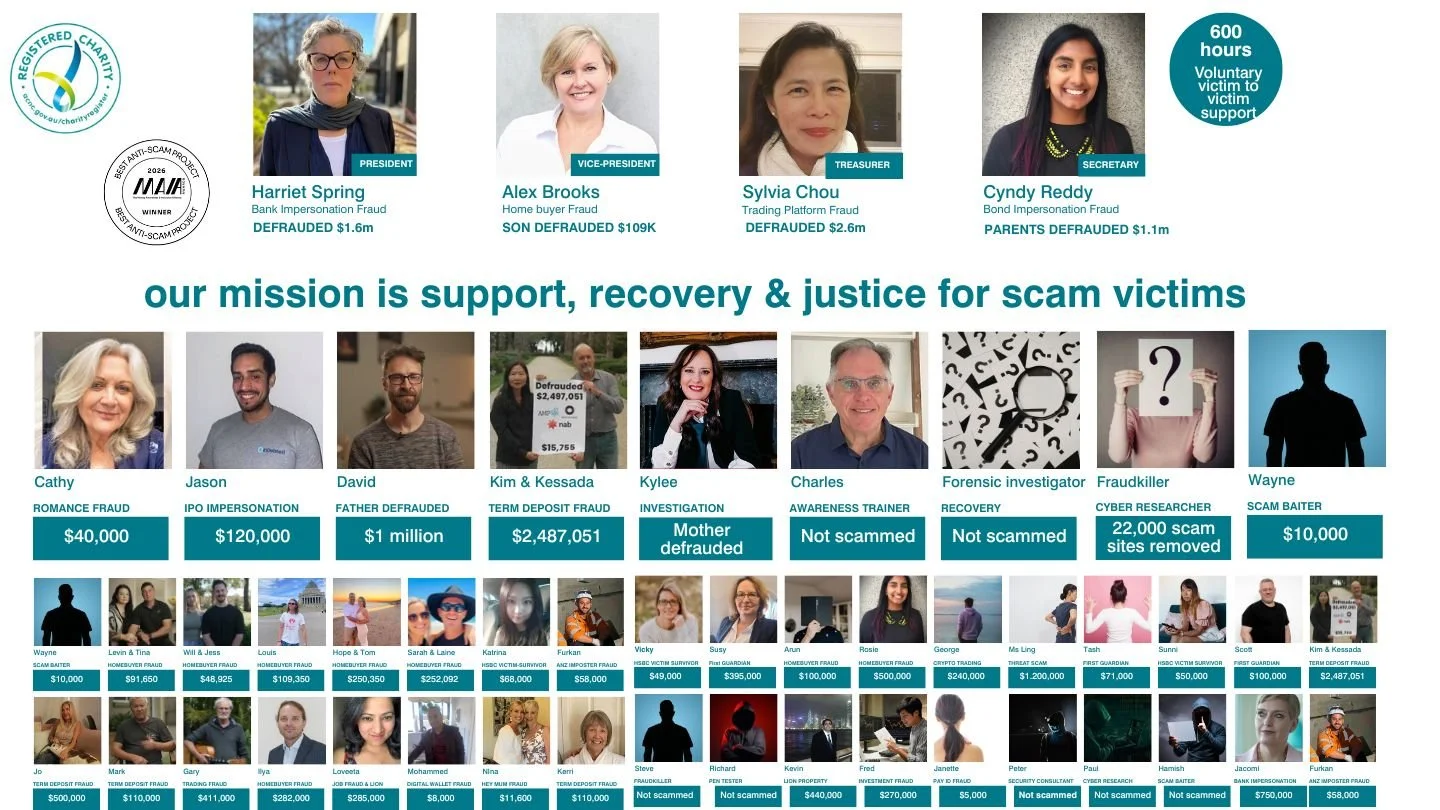

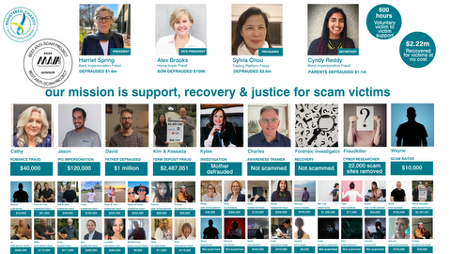

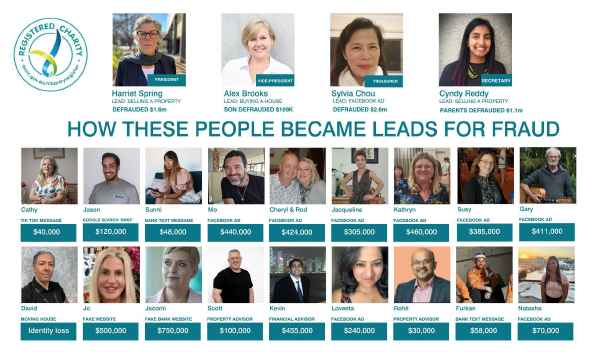

ABOUT SCAM VICTIM ALLIANCE

For more information Harriet Spring - President harriet@scamvictimalliance.org.au; Alex Brooks - Vice President alex@scamvictimalliance.org.au. Sylvia Chou - Treasurer sylvia@scamvictimalliance.org.au

Scam Victim Alliance is an ACNC-registered community of volunteer scam victim survivors and their loved ones offering support to victims needing support, recovery and justice after being scammed. We are the proud winners of the 2026 best anti-scam project in the Money Awareness and Inclusion Awards.

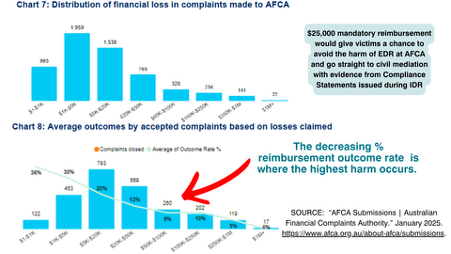

SOURCE: AFCA submission on the SPF in 2024

While the bulk of scam losses are at the lower end of the financial scale, AFCA’s own submission to the Scam Prevention Framework codes reveals that the higher the loss, the less chance there is of reimbursement

Scam prevention codes must save Australians from harm & trauma

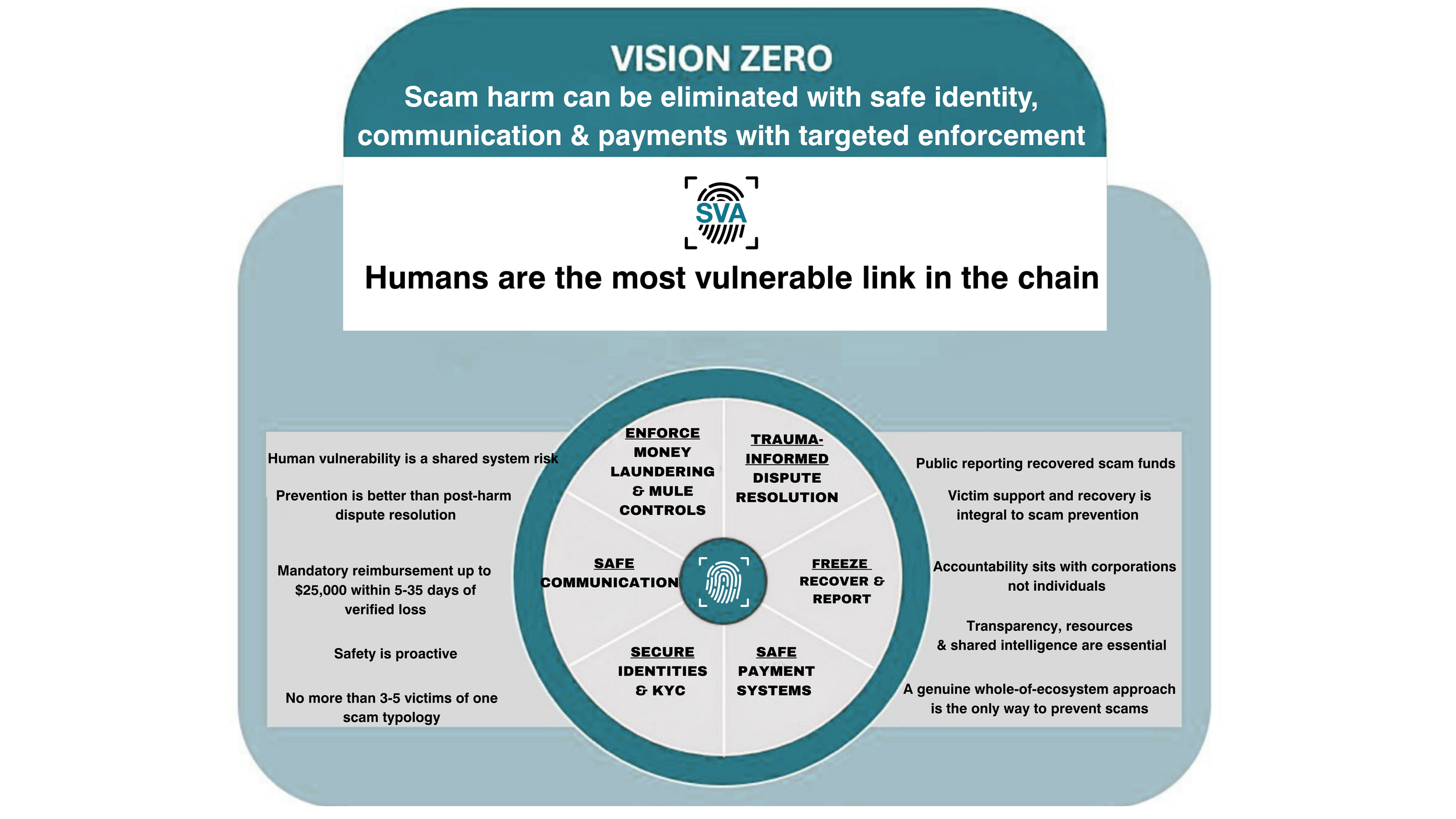

Scam Victim Alliance has a new submission to the Treasury’s latest consultation on the Scam Prevention Framework. Our submission argues that scams are driven by organised criminal networks that exploit regulatory loopholes and fragmented corporate responsibility. Building on our earlier recommendations—including $25,000 mandatory reimbursement, stronger scam intelligence, improved consumer education, and a Royal Commission into financial crime—it focuses on three priorities: preventing delays that allow criminals to exploit loopholes (particularly in email, online marketplaces and crypto ATMs), improving support for victims navigating Australia's complaints system, and adopting a "safe systems" approach that targets the underlying infrastructure of organised scam networks rather than treating scams as isolated incidents.

Australia's scam crisis is a failure of systems, with Governments caught unaware as to how fast, complex and industrialised fraud crime is. This submission explains how organised crime exploits gaps in regulation, why current responses are making the problem worse, and what Government, Treasury and industry could do to stop the harm from financial crime ruining people’s lives.

Executive summary

We are Australia's only self-funded, volunteer-led community, working directly to support victims through the complex harms global organised crime networks are wreaking on everyday citizens who trust their governments and banks to protect them.

We walk side-by-side with victim-survivors to deal with the overwhelming horror of financial crime, traumatic dispute resolution processes and broken enforcement systems in Australia.

Our ACNC-registered charity won the Best Anti-Scam Project of 2026 in the Money Awareness and Inclusion Awards. We helped consult with the United Nations Office on Drugs and Crime to develop the survivor-informed action brief to tackle fraud, which we implore the Government to implement.

We welcome the June 2026 Scam Prevention Framework (SPF) consultation, which rightfully shifts criminal responsibility onto corporations to prevent scams.

No country is untouched by the harm of scams, money laundering and illicit capital. Fraudsters, and corporate insiders typically scheme with other networked actors to specialise in finding the “legal loopholes” to commit deceptive fraud - please read Appendix H to understand the mechanics.

We stand by our January 2026 Scam Prevention Code submission, which included the following recommendations to protect Australians from the grave financial and psychological harm of scams:

1. All entities in scam chains must be designated and follow prescribed fraud controls, with instant reimbursement up to $25,000 for re-used scam infrastructure.

2. Scam education improvement with a hotline and Scam Infrastructure League Table publishing clear Scamwatch reported warnings to centralise and harmonise the system.

3. Regulators and law enforcement must detect scam infrastructure using regulatory and law enforcement subpoenas, compiling anonymised data for publication and transparency. Actionable Scam Intelligence is urgent and must begin immediately.

4. Mandatory IDR reimbursement up to $25,000 for verified scam losses paid within 5-35 days.

5. All designated sectors must have clear reimbursement, freezing and takedown obligations backed by infringement powers for recovery and be fined within 30 days of a breach.

6. A Royal Commission into financial crime with 6-year common law protections to apply to receiving banks.

This new submission to the SPF Treasury consultation focuses on 3 chief concerns:

SECTION 1 Delays in making the SPF operational risks the regulations and codes becoming a “scam proliferation playbook”, where schemers will develop more sophisticated scams - specifically exploiting gaps in failing to designate online marketplaces. crypto ATMs and email scams

SECTION 2 More funding is needed for victim support through horrific Australian Financial Complaints Authority (AFCA) External Dispute Resolution (EDR) processes, particularly given the court orders made in the ASIC v HSBC case.

SECTION 3 A ‘safe systems’ approach is needed to solve the scam crisis, with transparent investigative resources dedicated to scam typologies replicated across more than 3-5 cases - high value scam syndicate activity must go beyond ‘investment’ and ‘romance’ typologies to truly protect Australians.

Our community are all volunteers following our ACNC charter to support victims at no cost to victims experiencing the highest harm.

SECTION ONE: The SPF risks becoming a scam proliferation formula as criminals exploit loopholes

AUSTRALIANS EXPECT GOVERNMENT TO PROTECT CITIZENS FROM CRIME, NOT EXPOSE THEM TO BLAME & VICTIMISATION

Scam and fraud victims get more support from the government and law enforcement after being punched and robbed on the street than they do losing hundreds of thousands of dollars to elaborate deceptions and fraud perpetrated through banks or online and telco communication channels.

We applaud the SPF’s attempts to tie ‘controls’ to reimbursement but it is simply unacceptable that the “whole ecosystem approach” will no longer cover the top contact method for scams - email. Crypto ATMs are increasingly used only for scamming and we believe an immediate ban on these is required. Banks are increasingly debanking mules to protect themselves as the SPF begins, but there is an urgent need for humane intervention of exploited and gaslit mules such as the woman outlined in Appendix B of this submission. The danger of job and romance scams morphing into harmful threat scams means online marketplaces must also be captured by designations to prevent harm.

We acknowledge the SPF’s mention of impersonation controls and urge the Treasury to specify this more clearly. We are seeing phone calls impersonating trusted authorities morphing into dangerous threat scams as criminal networks pretend to be from the Australian Federal Police, ASIC or the

“A BANK THAT OPENS AN ACCOUNT WHERE MONEY IS BEING TRANSFERRED BY A FRAUDSTER IS AN ACCOMPLICE TO FRAUD. IT IS NOT A QUESTION OF WHETHER OR NOT A BANK CAN RECOVER THE MONEY … IT IS A QUESTION OF WHETHER OF NOT A BANK IS PERMITTING A FRAUD TO TAKE PLACE BY NOT KNOWING WHO THEIR CUSTOMER REALLY IS.” - the former head of Royal Bank of Scotland Sir Peter Burt[5]

Australian Tax Office and coerce people into giving up valuable personal information and payments. One victim was under the control of the scammer for 21 days, sharing intimate details of her location - including when she was going to the toilet. Her bank, Westpac, now charges interest on her scammed loss of more than $840,000.

Close the AI Scam Gap: Consumer vulnerability should be anticipated as criminal networks weaponise AI agents, data theft and frontier AI models

The emergence of frontier models and AI agents creates new risks for Australians under the Scams Prevention Framework. As AI systems increasingly search, recommend and execute actions on behalf of consumers, scammers will manipulate those systems through false signals, coordinated disinformation and impersonation. Consumers are the weakest link in this chain of harm. The SPF should explicitly require banks to assess AI-mediated scam risks - particularly impersonation - and implement safeguards while committing to share intelligence across sectors. AI platform designations should be considered now as a matter of urgency, along with designating crypto, email and online marketplaces, where harm is already entrenched.

SECTION 1: Key recommendations:

A “whole of ecosystem” approach to the SPF is nonsense if email is not designated. The key information on email vectors that needs to be part of compliance statements include:

Device, location and personal data on who created the email account used in any part of a scam

The email header information behind emails misdirecting payments

Which platform - Gmail, Microsoft and Yahoo are commonly used - allowed the scam email to be sent

How the email breach likely occurred (this is currently very difficult due to multiple vectors of breaches and insider threats)

If any other domain is behind the email, e.g. travel.io, then who registered the domain

A signed compliance statement from the financial firm, other professionals (e.g. lawyers) stating there were no data breaches or insider threats.

Online marketplaces have high harm from scam syndicate activity tricking people into complex payment scams or using their online searches as ‘lead’ vectors to target people for other threat, job or relationship frauds. The type of information that needs to be on compliance statements from these frauds includes:

Who created the social profile - the email and mobile number and location data associated with it

The external URL links used to trick or deceive a consumer

The bank/payment account tied to any payment offers or advertising accounts

Crypto ATMs need to be banned, given their proliferation in Australia. Victims using these machines deserve to be counselled through humane interventions that help them understand how muling works. These gaslit mules pose a difficult challenge that will require corporations debanking them to resource appropriately and safely as part of the SPF.

SECTION TWO: Delays until 2027 expose Australians to more trauma, blame and theft

AFCA EDR PROCESSES TRAUMATISE VICTIMS - REFORM IS URGENT

The delays to hearing cases relating to the SPF until March 2027 are unacceptable.

The uncontested June 18 Federal Court case ASIC v HSBC demonstrated banks do not lack knowledge of their broken scam controls but will delay redress and force consumers to absorb the consequences. A bank’s highest legal obligation is to protect their shareholders, not uphold consumer laws.

Furthermore, the way AFCA amplified and escalated the harm upon HSBC victims seeking help from the ombudsman requires an urgent Government review. AFCA forced HSBC scam victims to sign “shut up and go away” goodwill payments which have now put victims in a complex position if they signed restrictive deeds to receive less than 100% reimbursement. Scam Victim Alliance calls on AFCA to reopen HSBC cases with the new evidence heard in the federal court and issue public determinations on each case for transparency.

AFCA created extensive delays for HSBC victims before its “Mr T” determination was passed 13 months after the victim’s initial scam. Even with the win of this determination, other HSBC victims whose scam operated in slightly different ways - which is common amonst all scam typologies - were shamed for “releasing more than one OTP” to their scammers and therefore denied justice and fairness.

HSBC’s pattern of denying scam liability and shifting the blame to other vectors has been replicated by other banks, including ANZ who also had SMS spoofing scams that resulted in severe losses to their customers. ANZ even allowed their customers to be robbed by mules on ANZ platforms, and AFCA’s determination still blamed the victim while claiming Australian law forces the ombudsman to make these determinations.

THE SCAM DOESN'T HAPPEN JUST ONCE. IT HAPPENS OVER AND OVER AGAIN. FIRST, MULES STEAL YOUR MONEY. THEN YOUR BANK OR SUPER FIRM TELLS YOU IT’S NOT THEIR RESPONSIBILITY. THEN YOU ARE PUSHED INTO A LONG, EXHAUSTING AFCA PROCESS THAT TAKES MONTHS OR EVEN YEARS. NO-ONE FULLY EXPLAINS HOW TO BEST ARGUE YOUR CASE.- Taylor, 43, scammed of $420,000 superannuation in a complex ASIC-registered managed investment collapse.

Scam Victim Alliance contends that AFCA has been misinterpreting the existing protections against fraud in Australian legislation because it doesn’t have case managers with the skill needed to pursue the full reaches of its fairness jurisdiction.

Furthermore, when AFCA seeks external counsel to get legal advice on complex situations like scams, many corporate legal firms are also incentivised to insist to AFCA that existing fraud protections under legislation and common law are unclear, as their firms make money from providing more complex advice. It is Scam Victim Alliance’s belief that existing laws protect against mules and money laundering, but the Government and regulatory timidity has prevented this happening.

AFCA’s dogged insistence that Australia required law reform before it could do better for scam victims is not strictly true. Our experience of supporting victims through the AFCA process is that the ombudsman service regularly:

Forces complainants to negotiate against themselves.

Fails to explain the legal concepts at play in the complaint until the very end of negotiations, when AFCA case workers commonly bully and intimidate complainants into accepting lowball offers “because that’s all they will get”.

Doesn’t demand corporations share required information for complainants (particularly with CCTV footage), refusing to identify whether AUSTRAC suspicious matter reports or systemic issues have been escalated as part of the case.

Victims must have overwhelming evidence of financial firm failures to win their scam case at AFCA. Read the raft of different victim experiences at AFCA on Product Review to see the reality of everyday citizens’ experiences with the financial ombudsman.

Resolves scam complaints that total up to $2.6 million over a range of transactions, but not a single scam loss involving $1.2 million in one transaction.

Refuses to use its ability to waive interest on scam losses, forcing victims to be exploited by their banks for profit in complex cases.

AFCA is increasingly claiming it doesn’t have “jurisdiction” so it can get out of having to deal with complex scam cases, with new complaints being ruled out before they go to case management (where there are lengthy delays).

Many of our victim community report their case managers refusing to embrace the complexity of their case. Victims from non-English speaking backgrounds not only cannot understand the process but can rarely find the words to challenge the case manager’s limited understanding. This is why information transparency is so important.

AFCA case managers betray the organisation’s own fairness jurisdiction by refusing to see connected scam typologies and treating them consistently. The following three cases all involved in-branch handling of email payment misdirection of property settlements, yet had extreme differences in AFCA determinations:

Mr and Mrs C Panel Determination- reimbursed 70%.

Mr F Panel Determination - reimbursed 70% but not the $1800 a month interest NAB charged on the scammed loss.

Mr & Mrs D Non-Panel Determination - reimbursed $0 and has now had to spend $110,000 taking civil legal action.

In cases (a) and (b), there was an extra connection with ‘hidden text’ in the payment instructions revealing a Commonwealth Bank customer was unwittingly or knowingly part of the networked scam infrastructure - the fact that AFCA treats each case in isolation rather than a systemic failure requiring complainant compensation demands urgent review. Not all AFCA cases reach determination, particularly if the bank agrees to settle - in these cases, like in Levin Salaberry’s homebuyer email fraud - the bank will reach a confidential settlement and force the complainant to sign a restrictive deed. AFCA endorses this approach.

It is up to the Australian Government to demonstrate stronger leadership than simply accepting AFCA’s poor interpretation of existing common law, legislative and code protections against fraud. Delays to the SPF have put citizens and taxpayers in harm’s way.

We know that regulatory reform is challenging, but the SPF was supposed to be in place by the first quarter of 2025. It is ludicrous that ‘industry consultation’ has forced more losses on consumers during the last two years. In the case where the regulator ASIC took rare action against HSBC after overwhelming evidence the bank forced hundreds of consumers to take the blame for broken systems.

We urge the Australian Government to re-examine the successful elements of the United Kingdom’s mandatory reimbursement scheme, which would have most high-harm cases reimbursed within 2 weeks of a financial crime upending their lives. This will not only prevent consumer harm but also cost the industry less over time, by keeping disputes out of AFCA.

POOR REIMBURSEMENT OUTCOMES AT AFCA PUT AUSTRALIANS IN HARM’S WAY

“WHEN I WAS SCAMMED IN 2012, I GOT ALL MY MONEY BACK. WHEN I WAS SCAMMED IN A JOB SCAM, I RECEIVED ONLY $6,000 NON-FINANCIAL COMPENSATION FROM AFCA. WHEN RECOVERY COMPANY PAYBACK CONTACTED ME, I PAID THEM BECAUSE I DID NOT REALISE IT WAS A SCAM. I COULD NOT BELIEVE HOW BADLY AFCA’S FAILED PROCESSES PUT ME AT RISK OF THESE PREDATORS.” - Vaishali, 42, lost $25,000 to a recruitment scam and $3500 to Payback.

Scam Victim Alliance ally, psychologist Caroline Micallef (see Appendix C) notes that individuals and the Australian taxpayer unwittingly bears the cost of scam harm, which doesn’t show up as a direct cost measured by Scamwatch statistics:

“In the last six years I have seen clients who are experiencing trauma from financial scamming. This is a new cohort of clients who, when they first discover they have been scammed, the psychological response is acute and overwhelming. Some immediate reactions can be physical illness, breathlessness, a sense their world has collapsed and can represent the onset of what often becomes a prolonged psychological crisis.

Not only have they lost money but sometimes the most important relationship in their life (romance scams, their savings, their creditworthiness, and sense of self worth. Victims often find themselves cut off from family and friends. The feeling of shame can be so pervasive it prevents victims seeking assistance and can persist for years after the financial loss.

The psychological effects extend well after the incident. There can be lasting anxiety and difficulty trusting others. Another response is grief, for loss of money, their savings, their credit rating and most of all, self worth. Without timely intervention, victims are likely to develop greater symptoms and difficulties that add to the burden on mental health services, homeless services, acute medical services and community welfare supports.

”

Fraud and scams are A national economic security problem

The highest harm scam victims are those facing losses greater than the current proposed mandatory reimbursement of $3,000. Victims with higher losses undeniably face more complex scam typologies (with 11-15 different networked elements exploiting loopholes). Many Australian victims are unwittingly placed at risk of recovery scams due to the complexity and barriers of AFCA’s limitations.

The complexity and holes in coverage of the SPF risks baking in the existing inequity and information asymmetry, which is causing untold personal, financial and mental anguish to Australian consumers.

Scam Victim Alliance Treasurer Sylvia Chou, who lost $2.6 million in a complex scam that started with a Facebook ad and ended with banks profiting from her misery, was sectioned in a mental health facility. The greatest mental distress came during dispute resolution at AFCA, when she expected an ombudsman to see the crimes that had been perpetrated against her. The threat of bankruptcy also meant she would not be able to earn an income as an accountant.

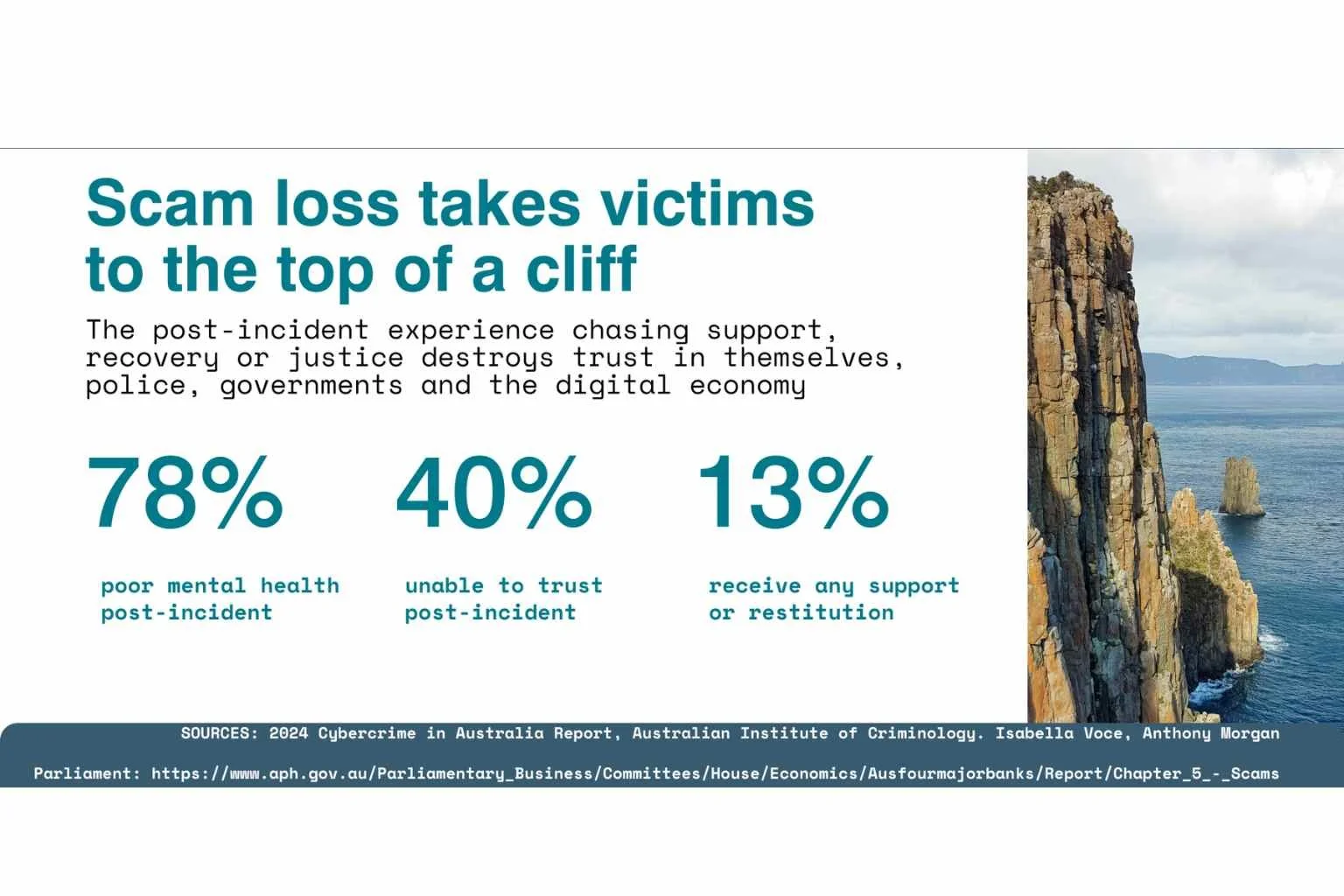

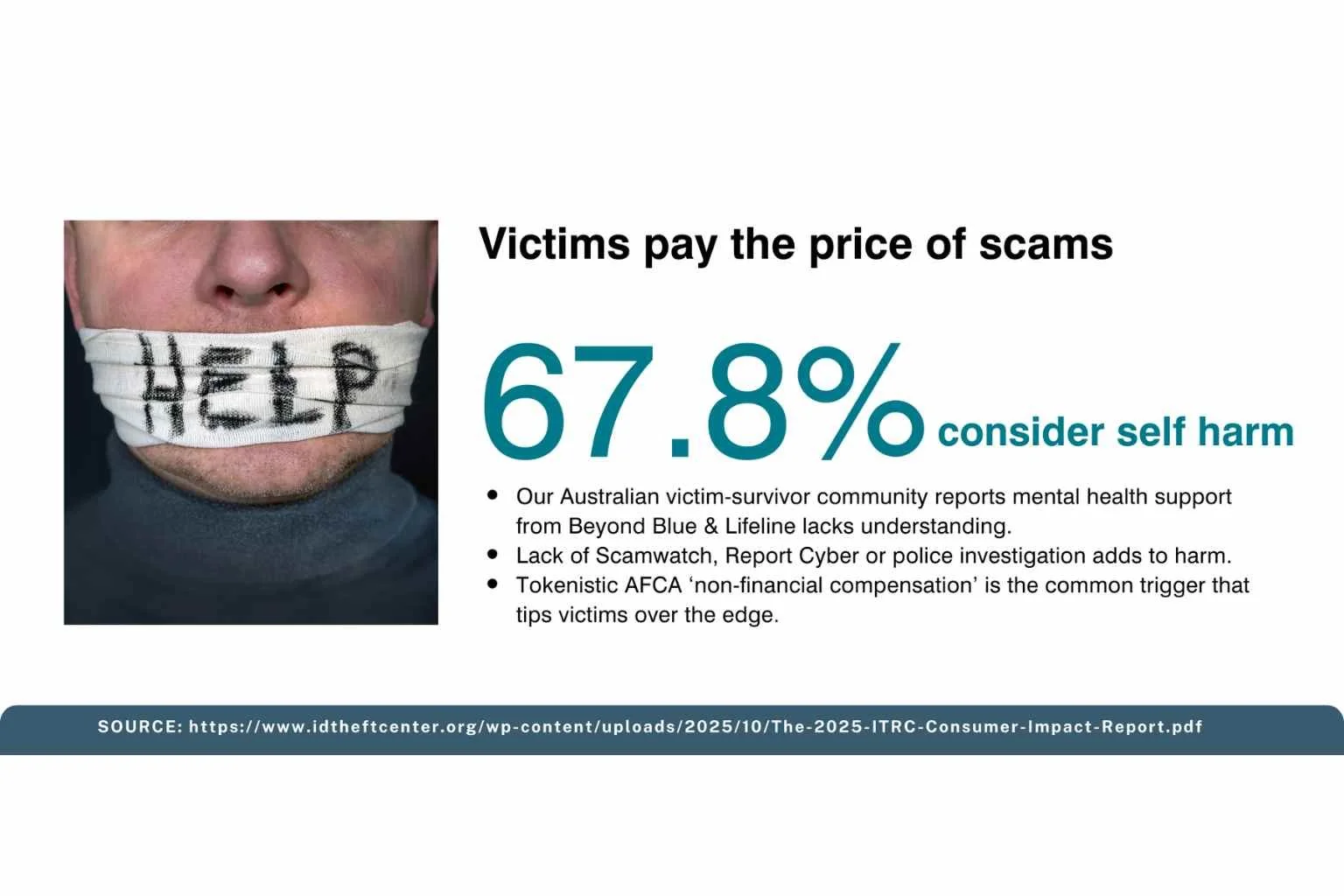

Most victims of high-loss scams face a long journey and legal battle, believing the initial scam is where the harm lies. It is only 3-6 months after their scam that victims realise they are in a constant state of anxiety and panic that is wearing them down mentally and emotionally. They hold out hope that AFCA’s dispute resolution can help them, only to realise very quickly that AFCA’s horrific processes blame and shame them for authorising their loss. We see this is the time when suicidal ideation and self-harm becomes a common experience in our victim community.

SOURCE: AFCA submission on the SPF in 2024

While the bulk of scam losses are at the lower end of the financial scale, mandatory reimbursement at $25,000 with full access to compliance statement evidence would protect victims from post-scam trauma harm.

Without considered pathways to de-escalate scams and fraud, Australia’s fragmented post-victimisation journey will continue to destroy savings, livelihoods and people’s trust in government and corporations.

If digital communication ecosystems continue being weaponised against citizens, this economic threat will quickly distort into a national security threat, too, where certain groups become radicalised forever.

“YOU JUST WANTED SOMEONE TO SAY SORRY FOR WHAT HAPPENED, BUT NOBODY DOES - THEY JUST BLAME YOU FOR AUTHORISING THE WHOLE STUPID THING.” - Frank, 72, a South Australian cancer survivor, lost $175,000 in a fraudulent property investment after moving his retirement savings due to concerns about “Trump’s war”. ASIC added the company to its Moneysmart Investor Alert List just four weeks after the scam

A mandatory reimbursement threshold of $25,000 will reduce costs for regulated entities over time by preventing thousands of low-value disputes from escalating into lengthy AFCA External Dispute Resolution (EDR) processes, which could cost multiple entities high determination fees.

We believe mandatory $25,000 reimbursement can help de-escalate the harm experienced by high-loss victims, as well as give them a starting point to decide whether to take their complex fight to civil courts and mediators, who may be better placed to deal with the situation.Mandatory reimbursement creates a stronger incentive for banks, telecommunications providers and digital platforms to invest in prevention, detection and disruption measures, as preventing scams becomes cheaper than managing disputes after harm occurs. It also reduces complaint volumes, administrative costs and reputational damage. A $25,000 threshold recognises that rapid intervention is more efficient than prolonged litigation-style processes. The UK experience shows that mandatory reimbursement is a stronger protective factor than having none at all.

Scam prevention should prioritise restoring consumers quickly and directing industry resources toward systemic risk reduction rather than costly post-harm disputes.

SECTION 2 SVA key recommendations:

Recognise the complex PTSD and harm scam victims in Australia face, and resource early intervention to stop the taxpayer bearing complex costs of scamming.

Reconsider delays to SPF and revisit the need to publish and share information with victims as part of a “safe systems” approach to resolving the scam crisis.

Harmonising and centralising scam prevention and investigation capabilities so victims can call one phone number to identify or report a scam (with language and translation for Mandarin, Arabic and Vietnamese language groups).

Ensure that mandatory reimbursement is re-examined to save greater costs and horrific delays by going through the AFCA process. We would be particularly keen to see a UK-style mandatory reimbursement scheme with a minimum $25,000 limit.

Understand that prompt and swift reimbursement avoids harm and will save Governments, corporations and taxpayers money over the long-term.

Consider funding complex AFCA cases with a “support fee” that corporations must pay in addition to other AFCA fees if case resolution takes more than 12 weeks at EDR.

SECTION THREE: Financial harm for high-loss victims is real and urgent

ASIC V HSBC HAS SET STANDARDS TO START OBLIGATIONS SOONER

The new consultation claims consumers are given IDR from 30 June 2026 and EDR from 1 January 2027, but there is no corresponding right for consumers to see or compare regulated entities' compliance performance before this time.

We contend the ASIC v HSBC Federal Court case demonstrates that some proposed SPF obligations may indeed have already moved beyond matters suitable for consultation.

We contend that the Federal Court case with HSBC may have created legal precedent necessary for stronger corporate controls to protect consumers. The Federal Court identified deficiencies in prevention, detection, investigation, remediation, governance and consumer restoration processes. The SPF should therefore distinguish between areas requiring innovation and those requiring mandatory baseline standards. “Reasonable steps” and principles-based flexibility cannot substitute for controls whose absence has already been judicially recognised as causing systemic consumer harm.

Comparing the Scam Prevention Framework with the Federal Court's findings in ASIC v HSBC

Flexible, principles-based obligations

Current SPF proposal

Flexible, principles-based obligations.

Federal Court finding

Some fraud controls are already objectively necessary.

Treasury could now examine

Introduce enforceable minimum standards before March 2027.

Scam intelligence sharing

Current SPF proposal

Better scam intelligence sharing, although Actionable Scam Intelligence is not yet clearly defined.

Federal Court finding

Financial institutions already possessed significant scam intelligence.

Treasury could now examine

Introduce mandatory reimbursement of up to $25,000 to create stronger incentives for industry prevention.

Industry capability

Current SPF proposal

Build industry capability over time.

Federal Court finding

Institutions had known about scam risks for years but failed to act transparently.

Treasury could now examine

Determine whether the real problem is a lack of intelligence—or a lack of enforcement.

Non-financial harm

Current SPF proposal

No recognition of non-financial harm.

Federal Court finding

The Court recognised non-financial harm in the Amended Joint Submissions on Liability and Relief:

"In the absence of those Key Controls, customers were at greater risk of suffering both financial loss and non-financial harm. Some customers did suffer those harms."

Treasury could now examine

Recognise human vulnerability as a system risk and introduce enforceable compensation for non-financial harm.

"Reasonable steps"

Current SPF proposal

Future-oriented regulation based on "reasonable steps".

Federal Court finding

Many minimum expectations have already been established by the Court.

Treasury could now examine

Create clear, transparent and enforceable obligations without requiring victims to pursue lengthy AFCA disputes.

Safe disruption powers

Current SPF proposal

Safe disruption powers.

Federal Court finding

Disruption itself can create consumer harm if poorly managed.

Treasury could now examine

Review and reform AFCA so dispute resolution no longer compounds victim harm.

The court’s orders to HSBC should now set the baseline for mandatory industry obligations, including AFCA’s oversight of previously determined cases. This is particularly important given the initial Government promises to roll out the SPF from the beginning of 2025. It is clear that delays have added to consumer harm and economic insecurity. HSBC victims are living, walking proof that this has occurred.

THE DISGUSTIFYING TRUTH OF BEING A SCAM VICTIM IN AUSTRALIA

One member of our community coined the word "disgustifying" to describe the moment she discovered the truth of how her bank, online social media and government failed to protect her. After draining her superannuation and making repeated payments through her bank to help her online partner "Alven" escape Syria, she learned that every dollar stolen had been funnelled through Australian banking money mules into what she now believes was accounts likely controlled by Africa’s ‘Yahoo Boys’ and scam networks. She had been tricked into taking out low-doc loans, which compounded her loss. The money she believed was saving the life of the online partner she had sent intimate photos to was instead helping fund what Interpol has described as a “global crisis” of human trafficking and other harms.

The SPF places significant obligation on industry but minimal new obligation on the Government to fund the investigative infrastructure required to pursue organised scam syndicates exploiting and weaponising Australian banking and communication infrastructure against citizens.

We believe there cannot be more delays in actionable scam intelligence and we need more regulatory capability to publish data around things like:

● Known mule bank accounts reported to Scamwatch, the Australian Financial Crimes Exchange, the Global Signal Exchange and state and federal law enforcement (this should be done regularly to help gauge how dangerous the banking system is for scams,

● Known spoofed telephone numbers used in previous frauds investigated by ASIC,

● Known accounts flagged to AUSTRAC through SMR and TTR reports that are associated with other known scam typologies.

We would also contend that part of the harm to victims is not adequately measuring scam losses or how effective warnings and education campaigns are. We would also ask the Federal Government to find a better way to measure the taxpayer impost of looking after scam victims after losing life-changing amounts of money.

Investment scams, superannuation fraud and the high-loss scams our victim community experiences do result in individual losses exceeding $100,000 and sometimes reaching more than $2,000,000. We have one particularly egregious case of a $6,000,000 scam.. These are more than opportunistic crimes - they involve scripted social engineering campaigns, professional money laundering networks and offshore coordination which evade the skill and capability of Australian regulators and law enforcement.

Home purchase fraud must also be recognised as a priority category. Property transactions in Australia routinely exceed $500,000 — in major metropolitan areas, frequently $1 million or more. Conveyancing scams, where criminals intercept communications between buyers, solicitors and conveyancers to redirect settlement funds, represent some of the largest single-victim losses in the scam ecosystem.

A first home buyer losing their deposit or settlement funds is not merely suffering financial harm. They are potentially losing decades of savings in a single transaction, with no prospect of recovery under the current framework and no realistic path to any meaningful redress.

These criminal attacks specifically target the conveyancing and legal sector, a largely unregulated scam surface under the current SPF. Email compromise at the point of settlement is a known, documented attack vector that has destroyed families financially and should be treated with the same investigative priority as superannuation fraud. Treating any of these crimes with the same resources allocated to a $500 parcel scam is problematic.

SECTION 3: SVA key recommendations:

SVA recommends the establishment of dedicated, properly resourced investigation units, with specific mandates covering:

● Large-loss investment fraud (individual losses exceeding $25,000);

● Superannuation scam syndicates;

● Home purchase and conveyancing fraud involving settlement fund diversion and laundering through gold, foreign currency and cash;

● Cryptocurrency-linked laundering networks connected to scam proceeds.

These investigation units should have direct access to AFCA complaint data, Report Cyber, ACCC Scamwatch reports and ASIC intelligence — with legal authority to act on cross-referenced leads without requiring victims to re-report through separate channels. It should report on recovered funds and make sure these are not put into general proceeds of crime pools, but dedicated to advancing protection and investigation of scams.

We would like to see Scamwatch offer a centralised service and co-ordinated phone line that gives victims realtime information on what is a known scam.

We believe a ‘safe systems’ approach is urgently needed - see Appendix E - How safe systems can help.

We believe Scamwatch needs to report the recovered scam money as well as scammed losses. Singapore now does this. Currently, Australian banks have no accountability to show those funds have truly disappeared and simply lie to AFCA and get away with it.

We know that JPC3 is working in cooperation with the AFCX and there have been successful intelligence sharing that now stops money leaving Australian shores - so why aren’t banks recovering more funds for scam victims? How can the Australian Government make the chain of custody more accountable to scam victims who simply cannot believe the lies they are told after they’ve fallen victim to criminals exploiting gaps in our systems.

Mandatory reimbursement leads to Scam Resilience: stronger together

The UK's 2026 Annual Fraud Report demonstrates why Australia's Scams Prevention Framework (SPF) must be built around systemic prevention and fund recovery with mandatory reimbursement rather than a slow and steady approach to ‘reasonable steps’.

Fraud is both an industrialised crime and a national security threat. In 2025, the UK recorded a record 4.06 million fraud cases, an 11 per cent increase on the previous year, with £1.28 billion stolen from consumers and businesses. On average, eight UK people were defrauded every minute and almost £2,500 was stolen every minute. Yet banks simultaneously prevented £1.68 billion in unauthorised fraud, stopping 70 pence of every £1 of attempted theft. In Australia, our banks will brag about their investment in anti-fraud measures while simultaneously blaming victims for authorising transactions into mule accounts hosted on their platforms.

The latest UK information shows the fastest growing scams are no longer traditional bank impersonation scams. Losses from investment scams reached a record £221.5 million, purchase scams £118.1 million, romance scams £39.2 million and advance fee scams £58.4 million. These scams overwhelmingly originate online, with 66 per cent of APP fraud beginning on digital platforms and a further 17 per cent via telecommunications channels.

The rise of elaborate deceptions around the globe demonstrates that criminals are increasingly exploiting artificial intelligence, impersonation, deep fakes, threats and social engineering rather than technical vulnerabilities. The SPF should therefore recognise that victims are not failing because they lack intelligence or awareness. Criminals are exploiting predictable human behaviours at industrial scale. Australia's response must move beyond consumer education towards enforceable, shared obligations across banks, telecommunications providers, digital platforms, dating applications, crypto platforms and emerging AI agents and a holistic supportive scam recovery pathway. We need law reform across the board to deal with fast-changing crime vectors.

ENDNOTES

1. “INTERPOL Report Warns of Increasingly Sophisticated Global Financial Fraud Threat.” Accessed June 20, 2026. https://www.interpol.int/News-and-Events/News/2026/INTERPOL-report-warns-of-increasingly-sophisticated-global-financial-fraud-threat.

2. “Scam Victim Alliance Winners 2026.” The MAIAs - Money Awareness & Inclusion Awards, n.d. Accessed June 19, 2026. https://www.maiawards.org/winners-2026/.

3. United Nations Office on Drugs and Crime. (2025). Survivor-informed action brief on combating fraud. United Nations. https://www.unodc.org/res/organized-crime/GFS/publications/UNODC_Survivor-informed_action_brief_on_combating_fraud.pdf

4. Scam Victim Alliance. “Scam Victim Alliance Urges 6 Changes to SPF Designations and Codes to Protect Australians.” Accessed June 21, 2026. https://scamvictimalliance.org.au/submissions-blog-updates/cash-mandate-submission-sva-d94mh.

5. “Cryptocurrency ATM Scams | AUSTRAC.” Accessed June 20, 2026. https://www.austrac.gov.au/general-public/cryptocurrency-atm-scams.

6. 7NEWS. “The Single Email That Cost an Australian Woman $732,000.” May 4, 2022. https://7news.com.au/business/property/wa-woman-loses-732000-to-property-scam-after-responding-to-fake-email-c-6674754.

7. Commonwealth of Australia Federal Court of. “ASIC v HSBC Bank Australia Limited.” Text. Federal Court of Australia, June 19, 2026. https://www.fedcourt.gov.au/services/access-to-files-and-transcripts/online-files/asic-v-hsbc.

8. Hussain, Ali. Pay out to Fraud Victims, Demands Ex Bank Chief. n.d. Accessed June 21, 2026. https://www.thetimes.com/business/companies-markets/article/pay-out-to-fraud-victims-demands-ex-bank-chief-qskv2rc55vv.

9. Scamwatch. “Scam Statistics.” Text. Australian Competition and Consumer Commission, April 8, 2026. Australia. https://www.scamwatch.gov.au/research-and-resources/scam-statistics.

10. “Determination For Case 12-00-1016692 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=f9f8941f-7379-ef11-ac20-000d3a6acbb4.

11. “Determination For Case 12-24-130239 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=ba8cf7fe-c58e-f011-b4cc-00224892c723.

12. “How AFCA Makes Decisions | Australian Financial Complaints Authority.” Accessed June 22, 2026. https://www.afca.org.au/what-to-expect/how-we-make-decisions.

13. ProductReview.Com.Au. “Australian Financial Complaints Authority (AFCA) Reviews.” June 14, 2026. https://www.productreview.com.au/listings/australian-financial-complaints-authority-afca.

14. “Determination For Case 12-00-1045764 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=add1b211-8384-f011-b4cc-002248112dcc.

15. “Determination For Case 12-00-1061026 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=8894dc11-27c4-f011-bbd3-7ced8da1919d.

16. “Determination For Case 12-00-1034883 · Customer Self-Service.” Accessed June 22, 2026. https://my.afca.org.au/searchpublisheddecisions/kb-article/?id=548b5513-5825-f011-8c4d-002248937998.

17. Content Renegade - Alex Brooks. Alex Brooks Asked MP Stephen Jones Financial Services Minister about Scams. 2024. 04:56. https://www.youtube.com/watch?v=2HZ9P36wg-A.

18. “One Year on: Impact of APP Reimbursement on Victims.” Accessed June 20, 2026. https://www.psr.org.uk/news-and-updates/latest-news/news/one-year-on-impact-of-app-reimbursement-on-victims/.

19. “Alert: Money Recovery Scam Using Fake Documents to Impersonate ASIC – Www.Payback-Recovery.Com.” News item. Accessed June 22, 2026. https://www.asic.gov.au/about-asic/news-centre/news-items/alert-money-recovery-scam-using-fake-documents-to-impersonate-asic-www-payback-recovery-com/

20. “Investor Alert List - Moneysmart.Gov.Au.” Accessed June 21, 2026. https://moneysmart.gov.au/check-and-report-scams/investor-alert-list#!impersonation-of-oakmere-capital-pty-ltd-oakmere-capital-com--4258

21. Australia, Commonwealth of Australia Federal Court of. “ASIC v HSBC Bank Australia Limited.” Text. Federal Court of Australia, June 19, 2026. https://www.fedcourt.gov.au/services/access-to-files-and-transcripts/online-files/asic-v-hsbc.

22. Duffin, Perry. “The Nigerian ‘Blood Cult’ Targeting Lonely Australians with Romance Scams.” Stuff, April 4, 2025. https://www.stuff.co.nz/world-news/360641133/nigerian-blood-cult-targeting-lonely-australians-romance-scams.

23. INTERPOL releases new information on globalization scam centres. Available at: https://www.interpol.int/en/News-and-Events/News/2025/INTERPOL-releases-new-information-on-globalization-of-scam-centres (Accessed: December 30, 2025).

24. UK Finance. “Annual Fraud Report 2026.” Accessed June 16, 2026. https://www.ukfinance.org.uk/policy-and-guidance/reports-and-publications/annual-fraud-report-2026.

25. “Are Technical Support Scams Getting More Advanced?” Accessed June 21, 2026. https://blog.gaborszathmari.me/are-technical-support-scams-getting-more-advanced/.

26. Scam Victim Alliance. “Deceived! An Investment Scam Nightmare for Sylvia Chou.” Accessed June 25, 2026. https://scamvictimalliance.org.au/victim-survivor-stories/scammed-silenced-and-still-fighting-sylvias-26m-battle-for-justice.

27. “Investor Alert List - Moneysmart.Gov.Au.” Accessed June 25, 2026. https://moneysmart.gov.au/check-and-report-scams/investor-alert-list#!gg-capital-group-limited-trading-as-bluelexus--1236 .

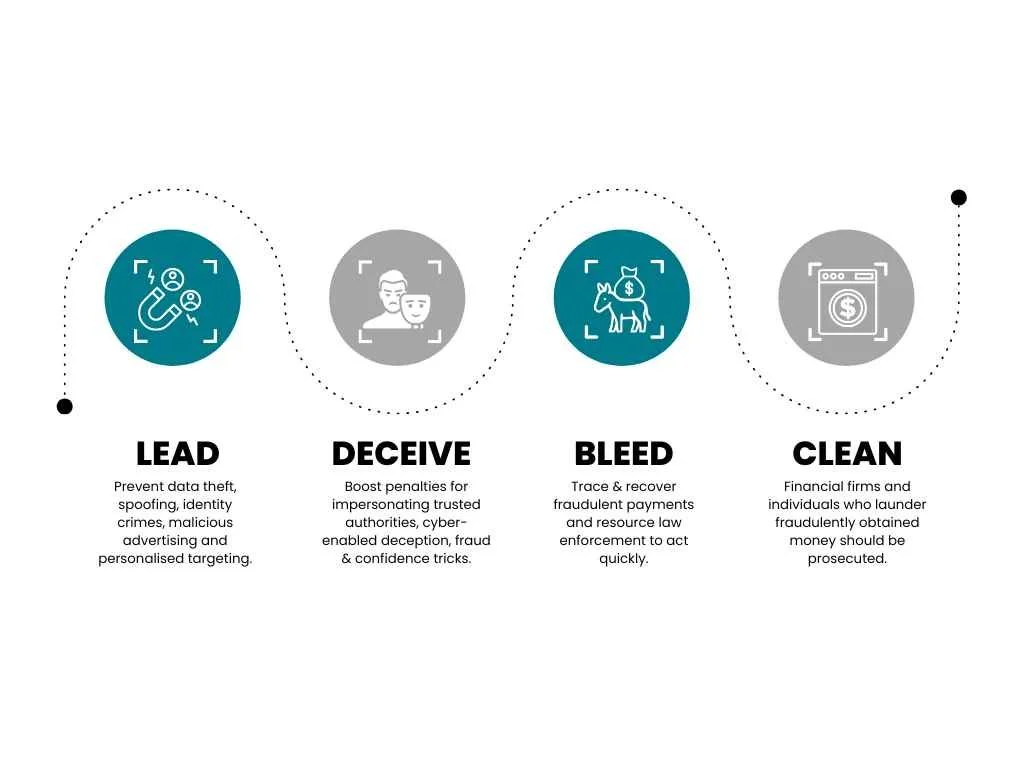

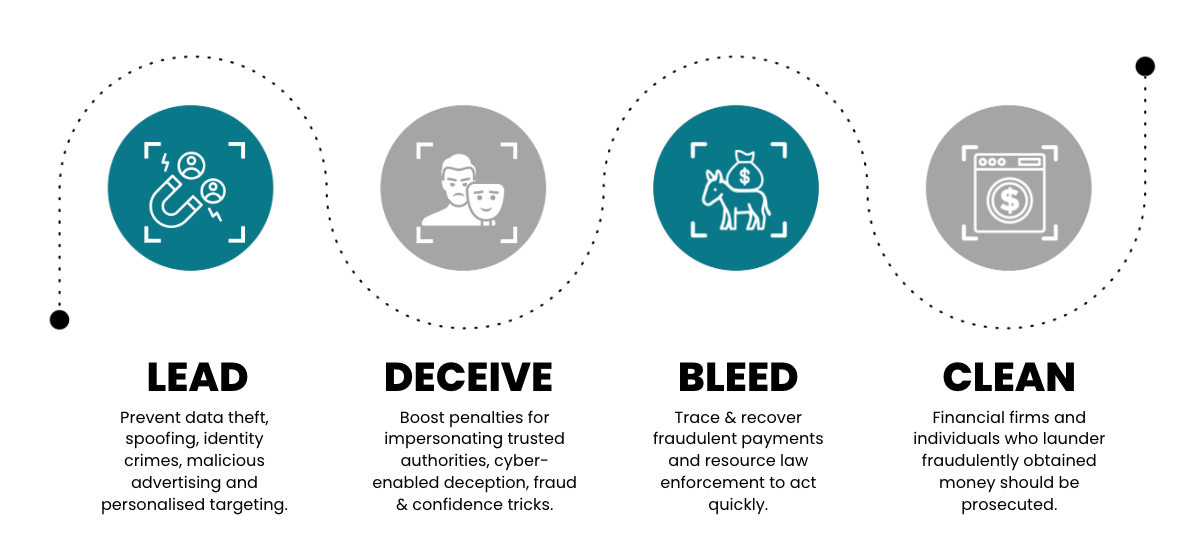

industrialised lead generation IS a financial crime blind spot

Scam Victim Alliance Every believes every major financial fraud follows the same pattern of LEAD-DECEIVE-BLEED-CLEAN. Victims are identified, profiled and nurtured long before they lose money or realise they’ve been defrauded. This submission argues that Australia's regulatory system focuses almost entirely on the moment money is stolen, while ignoring the industrialised lead-generation ecosystem that makes large-scale fraud possible.

Superannuation fraud is no longer primarily a consumer protection problem. It is a national economic security problem. The First Guardian, Shield and Australian Fidiciaries Ltd collapse of ASIC-registered managed investment schemes needs transparency and reforms to prevent more Australians losing their superannuation.

Executive summary

Scam Victim Alliance is a community of fraud victims supporting hundreds of Australians through the trauma that follows life-changing financial crime.

We welcome Treasury's recognition that lead generation sits at the beginning of the chain of events that can ultimately cause significant consumer harm.

Our experience suggests the problem may be larger than currently recognised, with “check your super” advertising thriving online.

Lead generation has evolved into the industrial front-end of organised financial crime and fraud. Today's criminal enterprises use the same advertising technology, behavioural profiling and customer acquisition techniques as legitimate businesses. Australians searching online to compare their superannuation, invest for retirement, recover scam losses or simply look for a new job can unknowingly enter sophisticated fraud funnels designed to identify, influence and eventually exploit them.

A compromised online banking login can reportedly be purchased for less than US$10. Digital advertising can then be used to identify and recruit thousands of potential victims at scale. Artificial intelligence is accelerating this process, making scams cheaper to run, more convincing and far harder to detect.

Australia's regulatory framework has not kept pace.

Our submission argues that lead generation should be viewed as critical financial fraud infrastructure rather than simply another form of advertising.

Unless governments regulate the beginning of the fraud journey, enforcement will continue to occur only after Australians have already lost their homes, retirement savings and financial security.

7 key Scam Victim Alliance recommendations to improve lead generation

Assume all Australians are targets for organised cybercrime as low-cost cybercrime-as-a-service offers shifts profit incentives towards criminal extraction of wealth from Australia’s legitimate banking and superannuation systems.

TAKEAWAY: Recognise fraud as an economic productivity and national security threat and respond quickly as AI and Quantum computing rapidly amplify the harm.

Ban algorithmic digital advertisingfor high-risk financial products, including scam recovery, comparing superannuation, investing, AI trading, creating SMSFs and “investing in property through your super”. Mandate that digital platforms, registered businesses and AI platforms retain advertising viewed against on user profiles to ensure victim redress and a successful ‘whole of system’ approach to preventing, disrupting and enforcing scams and fraud.

TAKEAWAY: Build technical capture and licensing requirements into lead generation and fraud facilitation - including ‘native content’ and ‘educational content’ and ‘website quizzes’ to ensure fraud victims can trace back the social engineering pathways after they have suffered a loss. It is critical that platforms capture and save financial services ads to be able to trace back which actors placed and profited from the lead generation and the downstream commissions.

Ban high-harm vehicles and facilitators for fraud such as weak auditors and crypto ATMs The best fraudulent schemes lay the groundwork over months, much like the First Guardian-Shield lead generation systems. Preventing the manipulation of Australians into believing a scheme is in their best financial interest is where the focus should be. Prohibiting social engineering through misleading online articles, website tools to “compare super”, “recover scam losses” or invest in “AI trading” used as lead capture unless independently verified and transparent with clear license numbers, with domain registrants also required to keep data on corporate entities..

TAKEAWAY: Introduce civil and criminal liability for professional facilitators — including lawyers, accountants, auditors, company formation agents, crypto ATMs, SMSF creators — who recklessly enable the creation and scaling of fraudulent financial schemes.

Adopt a victim-centred and ‘safe systems’ approach to fraud redress, including law enforcement follow-up, mandatory reimbursement and no-cost victim support through the Australian Financial Complaints Authority, as per Australia’s pledge at the UN Global Fraud Summit[1].

TAKEAWAY: Establish a national fraud strategy, similar to Britain’s Fraud Strategy 2026-2029[2] policy paper to guide a cohesive regulatory and enforcement approach

Ensure government identities cannot be forged to create more mule accounts which continue fraud harms. The Treasury must recognise the growing economic absurdity of identity fraud: leaked driver licence and passport credentials can be purchased online for under $10, while governments and victims bear replacement and remediation costs many times higher — often $30 or more for a driver licence and substantially more for passports and associated recovery processes.

TAKEAWAY: Australia should examine integrated anti-fraud identity models such as Singapore’s Singpass and MyInfo framework, which securely connects government identity verification with banks, telecommunications providers and regulated institutions in real time. A nationally coordinated digital identity ecosystem would significantly reduce impersonation fraud, mule account creation and document misuse while lowering long-term remediation costs for both governments and consumers.

Make fund recovery of fraud reportable and measurable. Singapore is already capturing this data[3] to measure how much of its citizen legitimate wealth is being hijacked by cybercrime to fund and scale further global crime harms.

TAKEAWAY: ACCC’s Scamwatch should report fund recoveries, not just reported scam losses. Australia should make fraud recovery rates formally reportable and measurable across banks, regulators and law enforcement agencies, recognising that stolen money is not simply an individual consumer loss but part of a global criminal economy that funds wider harms including human trafficking, child exploitation, drug trafficking and wildlife crime.

Hold a royal commission into financial crime and fraud. Australia should establish a Royal Commission into financial crime and fraud to examine the rapid industrialisation of scams, superannuation investment fraud, mortgage fraud, cyber-enabled theft and organised money laundering across the economy.

TAKEAWAY: Financial crime is no longer an isolated consumer issue — it is a growing national economic security threat. A Royal Commission would help expose the scale of organised fraud operating across Australia, identify systemic failures and build the coordinated safeguards, intelligence-sharing systems and accountability mechanisms needed to protect Australians from increasingly sophisticated transnational criminal networks, as Australia pledged at the recent UN Global Fraud Summit.

All Australians with money are ‘leads’ for malicious fraud schemes

Lead generation, cold-calling and other forms of ‘marketing’ create predictable pathways for fraud that begin long before any money is lost. Even before AI accelerated the disruption of financial services markets, consumers have long relied on Google searches, online ads, comparison tools and word of mouth advice from friends, as well as aggregators like Product Review or TrustPilot.

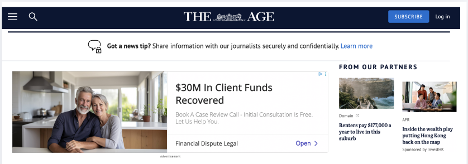

In a modern digital economy, individuals have their details and online cookies captured and passed along simply by reading legitimate commercial news websites. Scammers increasingly recruit victims through the same algorithmic advertising infrastructure that underpins Australia’s commercial news ecosystem.

Diagram (ii) Algorithmic ads on TheAge.com.au recruit leads for a range of businesses, both legitimate and illegitimate

Major publishers rely on a layered ad-tech stack—including content recommendation engines such as Outbrain and Taboola, programmatic ad exchanges like Google Ad Manager and supply-side platforms such as Magnite—which dynamically auction and optimise content placement based on engagement metrics. These algorithmic systems are designed to maximise click-through rates and user attention, not to assess the legitimacy of underlying content. As a result, scam actors can cheaply purchase targeted exposure and exploit behavioural profiling tools, which sell cheaply to the types of actors who orchestrated the First Guardian and Shield collapse.

Note that a ‘high value individual’ can be someone who is looking at content relevant to a major life event like trying to find a new job, getting married, having a baby, moving house, planning retirement or looking to invest. All of these life events are ‘leads’ for malicious industrialised fraud actors who have breached Australia’s trusted infrastructure (such as the Penthouse Syndicate inside NAB).

This creates an environment where fraudulent investment ads, impersonation content, and other scam vectors are distributed at scale alongside legitimate journalism. The fragmentation of responsibility across multiple intermediaries further weakens accountability, enabling scammers to rapidly test, iterate, and optimise deceptive campaigns in ways that mirror legitimate digital marketing practice, where algorithmic advertising ramps up the harms.

Evidence from the First Guardian and Shield collapse Facebook and Google ads highlights how industrialised and algorithmic lead-generation ecosystems create the on-ramp for large-scale financial harm. Testimony indicates the existence of organised “lead gen” networks in Queensland and Victoria spruiking website landing pages that got people to ‘check their super’ or ‘compare their super’. Actors from these schemes have told Scam Victim Alliance that between $20m and $40m was spent on digital ads over several years recruiting the 10,000 to 12,000 people who later lost money to these schemes.

The First Guardian and Shield loss experience further suggests that regulators can only detect misconduct after funds have been misappropriated. The collapse of Australian Fiduciaries Ltd followed a similar pattern, with nurses particularly exposed to the ‘lead-engage-convert’ model spruiking collapsed NDIS property schemes that enriched multiple .

The challenges experienced by consumers seeking redress through mechanisms such as the Australian Financial Complaints Authority, the Compensation Scheme of Last Resort, the CDDA or Act of Grace discretionary schemes highlight a deeper structural issue that requires urgent resolution.

There is a massive accountability gap for regulators, government agencies and trusted corporations holding credit, investment and other financial services licences while redress for harm remains limited and fragmented. When harm arises from lead generation practices that fall into regulatory grey areas, agencies and corporations will never be seen to have breached a specific duty.

When consumers can suffer significant financial loss without access to meaningful redress, it means our regulatory and enforcement frameworks do not adequately capture the early-stage conduct that set the harm in motion. This misalignment between how harm actually occurs and how responsibility is assessed underscores the need to bring lead generation activities more clearly within the regulatory and enforcement perimeter.

Strengthening oversight of lead generation is therefore not only a preventative measure, but a necessary step to restore accountability across the system. By clearly defining when lead generation activities constitute a financial service, extending obligations to those who influence consumer decision-making, and addressing incentive structures that prioritise conversion over suitability, the regulatory framework can better reflect the realities of how financial harm occurs. Without these reforms, compensation schemes will continue to struggle to deliver outcomes for affected consumers, as the origin of harm remains structurally disconnected from the points at which responsibility is currently assessed.

Artificial Intelligence is scaling harm

Artificial intelligence is improving efficiency across the financial system, but also amplifying risks like synthetic identity, misinformation, disinformation and fraud. Our community has lived experience (and large financial losses) which show structural apathy, political inertia, and financial institutional design failures are scaling the financial harm.

Consumers are often presented with promotional content that mimics trusted guidance, without clear, consistent or comparable disclosure of commercial intent, remuneration structures, or the risks associated with the recommended actions. By the time an unwitting consumer is on a call with an adviser or lead generator, they are already primed to accept bad advice.

Digital platforms have enabled the large-scale use of low-cost, algorithmically targeted advertising to circumvent longstanding protections such as bans on cold calling. Our engagement with victims involved in recent collapses such as First Guardian, Shield, Australian Fiduciaries Limited and Lion Property indicates that this ecosystem remains active. Advertisements across platforms such as YouTube and Facebook continue to funnel consumers into conversations with entities functioning as lead generators, operating under business models driven by switching fees and downstream commissions. These interactions frequently lead consumers toward complex and high-risk strategies—including SMSFs, leveraged property investment, scam recovery or speculative offerings—without the benefit of clear, standardised, and consumer-tested disclosures that would enable genuine comparison or informed consent.

Meanwhile, the corporations at the heart of these schemes also seem able to set up property developments and managed investments that also defraud banks and other finance companies by double-mortgaging assets that have little to no regulatory scrutiny. This submission calls for urgent reform: banning algorithmic ads for high-risk products, mandating licensing and vetting of all promoters, prohibiting deceptive comparison platforms, and adopting victim-centred enforcement including restitution and protections from further penalties.

OXIL research shows scam and fraud targeting is now based on situational vulnerability

Large-scale analysis of scam activity shows that modern fraud is not random but engineered. Lead generators build trust through a ‘funnel’ that starts with a signal of intent from a vulnerable consumer. Digital platforms succeed at not simply marketing, but also scaling systems in which individuals are identified, filtered and engaged at moments when they are most susceptible to influence.

By leveraging personal and behavioural data, lead generation systems are able to prioritise those most likely to respond, effectively targeting vulnerability at scale. These systems operate using a combination of broad exposure and targeted engagement. Consumers may first encounter generalised advertising, but are quickly funnelled into more personalised interactions that build trust and momentum over time. This creates industrial-scale pipelines of potential victims, where influence is applied progressively rather than at a single point of decision. By the time a financial product or investment opportunity is presented, the individual has often already been psychologically primed, making the eventual decision appear voluntary while being shaped by earlier interactions.

When engagement, phone calls and relationship building is driven by repeated exposure, emotional cues and tailored messaging, traditional notions of consent—such as clicking on an advertisement or opting in to be contacted—do not reflect genuine understanding or agency.

This means the Treasury must urgently support a shift in regulatory approach. Rather than placing responsibility primarily on individuals to identify and avoid harm, there is a clear need to recognise lead generation as part of the broader harm pathway. This requires a safeguarding model that addresses risks earlier in the chain, ensuring that systems capable of identifying and influencing vulnerable consumers are subject to appropriate oversight, accountability and intervention.

Fraudsters have been emboldened by Australia’s weak approach to enforcing the law or addressing cyber-enabled financial harm. Fraudsters can use technology, fake identities, social media and sophisticated financial schemes to steal billions from ordinary Australians every year. These crimes hurt families, destroy retirement savings and weaken trust in banks, government and the financial system itself.

Scam Victim Alliance contends that improving identity protections, stopping dangerous advertising practices, holding facilitators accountable and building stronger cooperation between banks, regulators and law enforcement, Australia can make it much harder for organised fraud networks to operate. We believe money laundering laws can be used more effectively to stop the harm.

Fraud prevention should not depend on ordinary people spotting highly sophisticated crime on their own. Australia needs safer systems, faster action and stronger accountability before more people lose their homes, savings and futures.

Endnotes & references

Scam Victim Alliance. About Scam Victim Alliance.https://scamvictimalliance.org.au/about

Voce A, Morgan A. The Costs of Serious and Organised Crime in Australia. Australian Institute of Criminology, 2025.

Reserve Bank of Australia. Financial Stability Review: Financial Stability Implications of Artificial Intelligence. September 2024.

United Nations Office on Drugs and Crime. Global Fraud Summit 2026 Pledges.

UK Government. Fraud Strategy 2026–2029.

Ministry of Home Affairs (Singapore). Scam Loss Recoveries in the First Half of 2025.

Dastoor C. Calls to Fix Shield, First Guardian Anti-Hawking Loophole. Professional Planner, 20 August 2025.

Taylor C, Taylor A, Sutherland J, Hakmeh J, et al. Rethinking Scam Prevention: Large-Scale, AI-Powered Analysis for a Safeguarding Approach. Oxford Information Labs.

Taylor, Carolina Caeiro, Alice Taylor, James Sutherland, Joyce Hakmeh, Emily. “Rethinking Scam Prevention: Large-Scale, AI-Powered Analysis for a Safeguarding Approach - Research.” Oxford Information Labs. Accessed April 20, 2026. https://www.oxil.co.uk//research/rethinking-scam-prevention-large-scale-ai-powered-analysis-for-a-safeguarding-approach.

SVA Speaks out about scam prevention framework codes

Scam Victim Alliance has 6 key recommendations to stop Australia entrenching the harm of scams in response to Treasury’s SPF codes and designations.

Scam Victim Alliance spent our Christmas holidays writing this submission to Treasury about it’s world-leading reforms to fight scams. The SPF risks becoming a framework of good intentions that will actually increase scam harms unless the Codes impose clear and enforceable obligations on regulated entities

Executive summary

Our lived experience gives us deep insight into how scammers manipulate digital payment systems — and how banks, telcos, and digital platforms have allowed their infrastructure to be weaponised. Australian corporations are unwittingly funding what Interpol has called a “global crisis” of human trafficking and other criminal harm. We welcome this opportunity to make a submission to the SPF Treasury consultation.

Scam Victim Alliance (SVA) was founded in May 2025 to support Australians devastated by scam frauds, abandoned by a system that delivers inconsistent recovery processes and untold trauma.

Scam fraud hits hardest in Australia’s most vulnerable communities—older Australians and those from culturally and linguistically diverse (CALD) backgrounds—forcing taxpayers and individuals to carry the cost of the escalating scam fraud crisis harming all nations around the globe. Australia now faces scam compounds setting up shop on its doorstep—in Timor-Leste, New Guinea, Palau and Fiji, no doubt attracted by the rich pickings of Australia’s poorly protected payments markets.

We believe that if the clear recommendations from the 2019 Banking Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry had been successfully implemented and enforced by APRA and ASIC, much of the scam-related harm experienced since 2020 could have been significantly reduced, as detailed in Appendix A. If scam losses and their downstream impacts were properly accounted for, the true cost to taxpayers would be staggering.

For example:

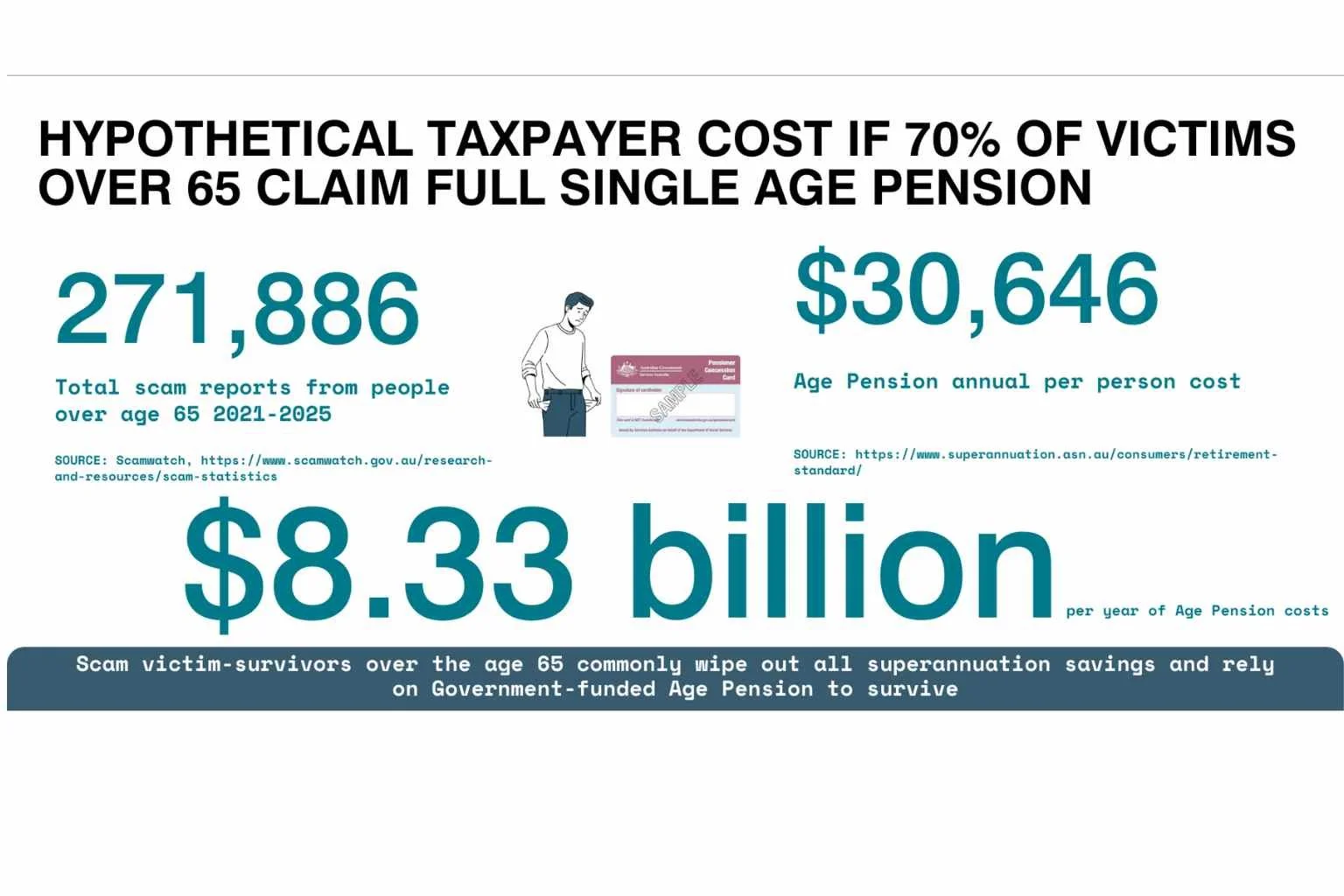

● Since 2019, 272,000 Australians over 65 have lost their superannuation to scams. If just 70% of these people had to then claim an Age Pension due to not having any superannuation, this would add an estimated $8.33 billion annually to Aged Pension costs.

● And if just 70% of Australia’s estimated 1.25 million scam victims since 2021 required Medicare-funded psychological support, it would cost taxpayers approximately $1.24 billion in mental health care.

Our executive summary recommends key inclusions and designations to stop scams proliferating and make a genuine attempt to reimburse consumers.

These costs represent real and growing pressure on Australia’s public services, all while institutions that failed to prevent scam fraud are not held financially accountable.

In addition, we believe two critical failures have left Australians exposed to an untested legal liability that’s enabled large-scale theft from individuals through scams:

1.Banks have refused to acknowledge that their platforms and processes have been conduits for criminal fraud.

Banks have remained wilfully blind to their role in the fraud crisis, relying on the same strategies of denial used during the 2019 Royal Commission. Banks and payment platforms deflect from their facilitation of fraud (including impersonation and payer manipulation fraud) by insisting that scam losses are customers’ fault, even though banks have legal duties:

not to allow mule accounts to be established that don’t meet Know Your Customer (KYC) standards,

raise red flags for known scam patterns,

transparently recover scammed funds.

Banks spend millions marketing their “scam defences” and boasting about AI and staff investments — yet still blame customers when their own processes and failures to train staff on known scam typologies fail. Banks have ignored basic safeguards like 48-hour payment holds or MFA for high-risk transfers, such as property purchases or superannuation, and shifted the blame to customers rather than invest the paltry $100m needed to establish CoP before the fraud crisis escalated in 2020.

2. Regulators and Government failed to implement Confirmation of Payee (CoP) as part of the ePayments Code review early enough to protect Australians.

In 2019, Consumers Federation of Australia called out the lack of “meaningful sanctions to create an effective deterrent for non-compliance” in the ePayments Code, leaving Australians uniquely exposed to fraud. The ePayments Code - along with the Banking Code - are sometimes contentiously misinterpreted by an over-run External Dispute Resolution body, the Australian Financial Complaints Authority (AFCA).

In Part 2: Introduction of this submission, we outline how corporate failures have emboldened domestic fraudsters to escalate their tactics. In Part 3: Consultation questions we specifically explain the 6 key recommendations outlined in our Executive Summary below and in Part 4. Whole of ecosystem approach we offer our conclusions. Evidence for our recommendations is then provided in our Appendix items.

We welcome the draft Scam Prevention Framework (SPF) and newly published codes and designations which promised: “Victims will have clear pathways to compensation if the business fails to meet robust standards.” — Former Assistant Treasurer Stephen Jones on 13 February 2025 when he promised the SPF Codes would protect Australians and be operational from July 1 2026

Upon release of the designations from Treasury, analysis published in Australia’s leading financial newspaper stated:

“The definition of reasonable steps is rubbery enough to give the banks, telcos and social media platforms a “get out of jail free” card … Compounding that problem is the fact there will be no legally enforceable actionable scam intelligence for at least two years.” — Australian Financial Review’s Tony Boyd on 22 December 2025 about the newly released Treasury consultations and position paper this submission focuses on

SVA believes individual victims and taxpayers bear the cost of financial crime that corporations profit from. We believe the SPF designations must be significantly improved with 6 recommendations.

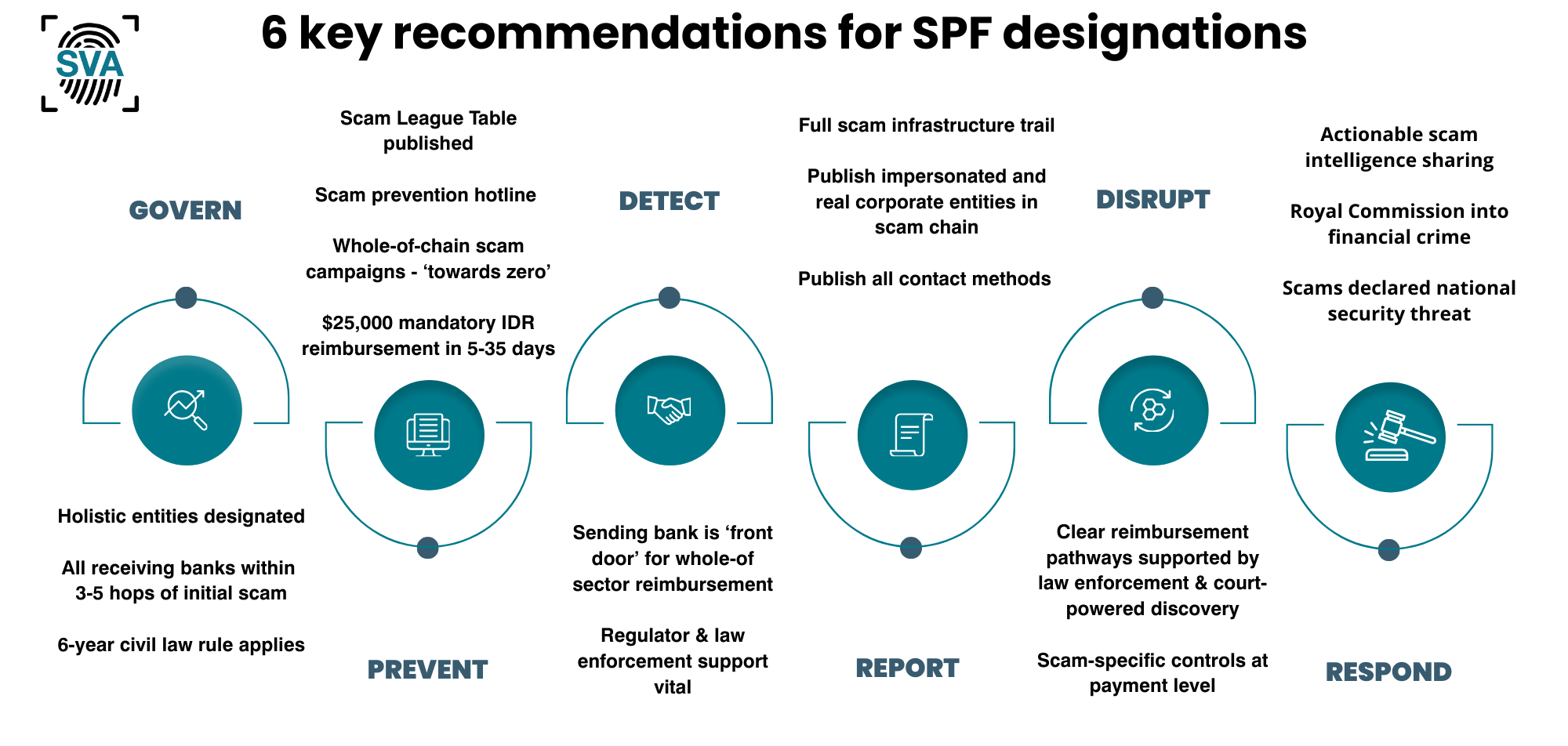

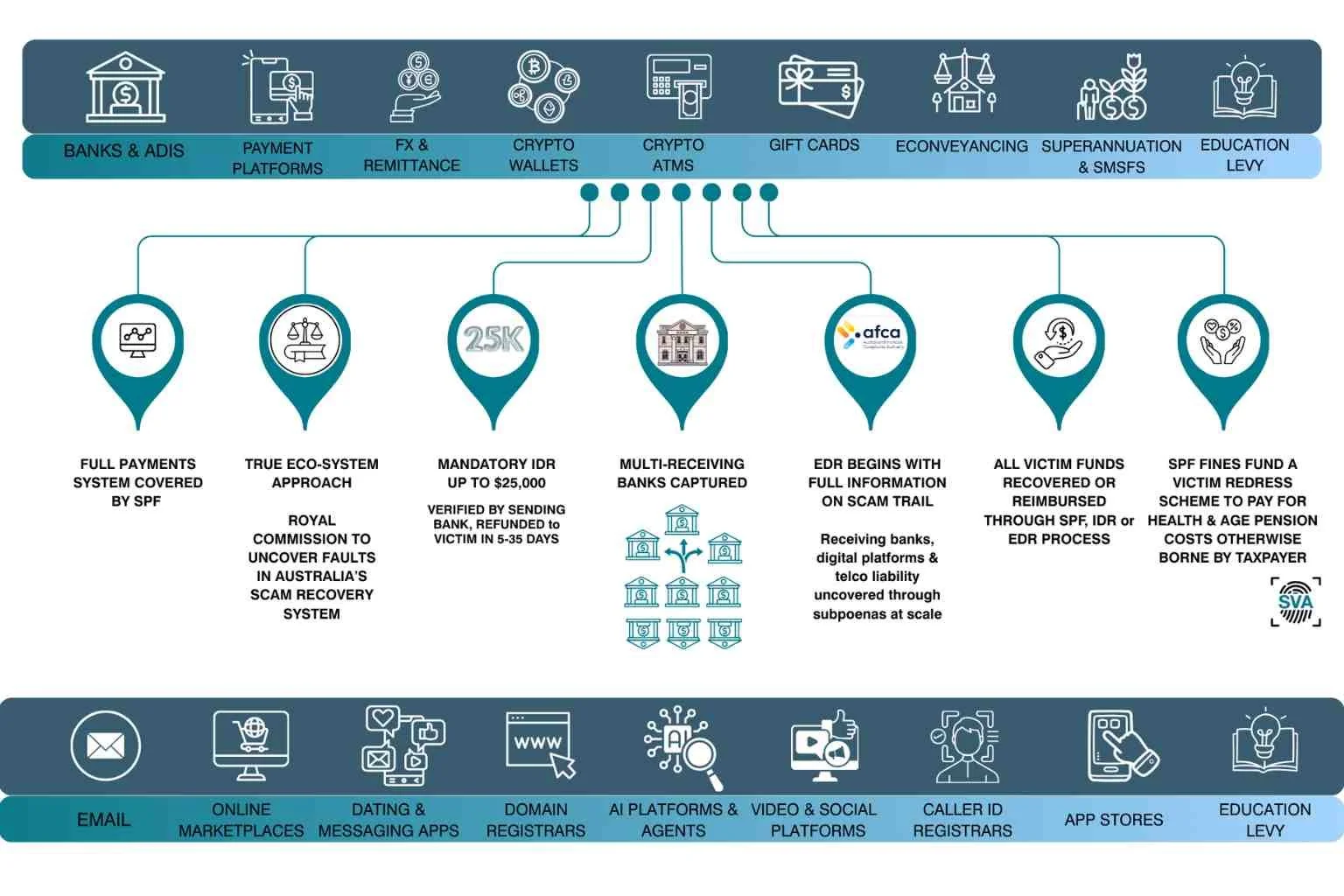

Recommendation 1. Governance works only if all entities in scam chains are designated

All relevant sectors must be designated under the SPF to ensure whole-of-ecosystem accountability and give the framework any chance of achieving its policy intent. This includes:

● Banking & Payments: All ADIs, non-bank remitters (especially foreign currency remitters such as Wise, Revolut or OFX), cryptocurrency exchanges and ATMs, eConveyancing platforms (PEXA and Sympli), gift card services, payment providers (BPay, PayID, Monoova, Cuscal, PayTo etc), and superannuation funds.

● Digital Platforms: Email hosts (e.g. Gmail, Outlook, Yahoo), online marketplaces (Meta, Gumtree, eBay), dating apps and platforms (Tinder, Hinge etc), domain registrars (e.g. GoDaddy, Ventra IP), Hosting platforms (e.g AWS or entities responsible for servers not serving illegal material), Caller ID registrants (e.g. Hiya), AI agents (e.g. ChatGPT, Claude, Gemini), App stores (side-loading malware is a key scam vector).

Furthermore, we believe that ASIC’s Registers and MoneySmart Investor warnings must be held to the same standard as the SPF dictates for regulated entities. Our community believes ASIC’s investor warnings have failed to keep up with known scam patterns and actively endangered people to invest in imposter and investment scams that could have been prevented through up-to-date warnings and a hotline to check for known scam types.

Additionally, an education levy should apply to designated sector ASIC registrations to fund a Safe Systems approach to scam awareness.

The SPF risks becoming a framework of good intentions that will actually increase scam harms unless the Codes impose clear and enforceable obligations on regulated entities.

The proposal for equal apportionment of scam-related compensation among institutions is problematic. Banks have historically borne the responsibility for safeguarding customer funds. Diffusing bank liability must be tied to demonstrated levels of responsibility and control failure—not arbitrarily split. Without enforceable standards and fair redress mechanisms, this framework will not only fail to protect Australians, it will entrench systemic gaps and allow industry actors to continue passing the cost of preventable fraud onto victims and taxpayers.

Recommendation 2. Prevent scams with a hotline and Scam Infrastructure League Table in advance of Actionable Scam Intelligence-sharing

A scam education campaign and consumer hotline should be funded through an ASIC levy on all SPF-designated entities or funded by proceeds of crime. Scam infrastructure reporting must begin in the first half of 2026 with the NASC publishing a Scam Infrastructure League Table, updated quarterly, listing the most misused corporate brands (including impersonations of government entities like the Australian Tax Office), mule accounts, phone numbers and scam ad, email and website tactics — with strict liability for entities failing to block repeated abuse. Consumers must be able to call a hotline to find out if they are paying a known scam account, receiving calls from a known scam number or receiving ads, emails or phone numbers from known scam compound devices or locations.

Furthermore, scam infrastructure data can already include existing intelligence like:

● Known mule accounts reported to Scamwatch, the Australian Financial Crimes Exchange, the Global Signal Exchange and state and federal law enforcement information,

● Known spoofed telephone numbers used in previous frauds investigated by ASIC,

● Known accounts flagged to AUSTRAC through SMR and TTR reports that are associated with other known scam typologies.

We would also contend that part of the harm to victims is not adequately measuring scam losses or how effective warnings and education campaigns are. We would also ask the Federal Government to find a better way to measure the taxpayer impost of looking after scam victims after losing life-changing amounts of money.

Recommendation 3. Detect by having sending banks as single ‘front door’ for whole-of-sector reimbursement, supported by regulators and law enforcement

Banks are best placed to act as the front door for scam reporting, verifying losses with their customers before collecting full scam infrastructure data (e.g. malicious ads, email headers, hosts of illegal content, mule accounts, fake domains, impersonated brands) to help detect patterns and trigger liability across non-bank sectors. Regulators and law enforcement would support this scam infrastructure reporting.

Recommendation 4. Report full scam payment‑trail disclosure to trigger a 5-35 day IDR reimbursement up to $25,000 with funds recovered from other SPF entities through infringement notices and court enforcement.

Banks must verify scam losses and pay up to $25,000 at IDR within 5–35 days. If a case is unresolved, regulators and law enforcement must subpoena the full scam trail - including scam infrastructure and receiving banks - before escalation to EDR or recovery from other sectors.

SVA recommends the full scam infrastructure trail must be subpoenaed quickly (ideally by day 36 after the scam report if mandatory $25,000 IDR reimbursement fails) to trigger early detection and disruption. Strict liability must apply to any entity that fails to block or shut down known scam infrastructure. All SPF fines should fund a victim redress scheme to fund ongoing reimbursement and mental health programs.