Economic reform roundtable submission

Financial crime is a severe handbrake on productivity

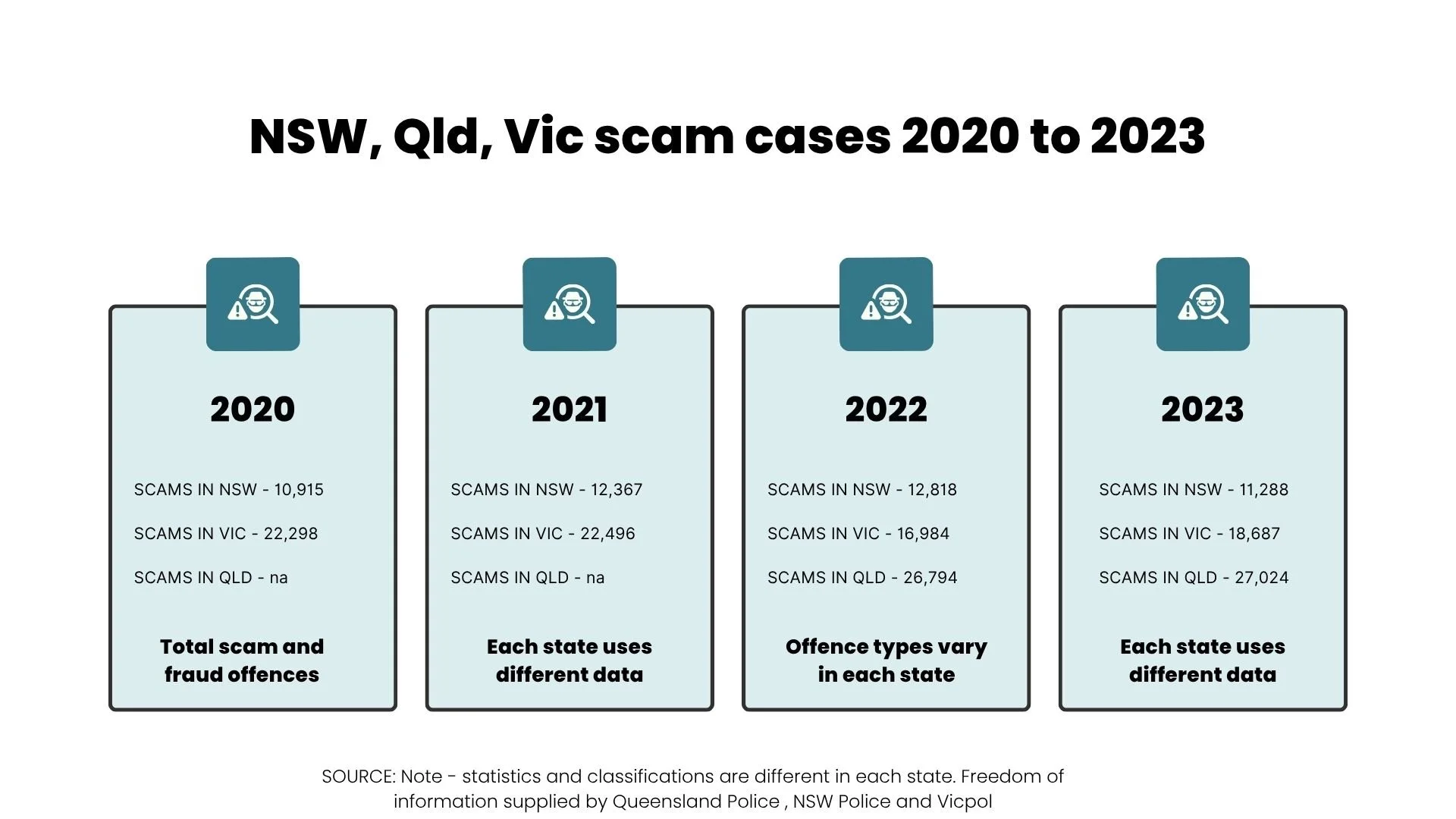

The Scam Victim Alliance (SVA) is a not-for-profit community of survivors of cyber-enabled fraud and scams. We welcome any chance to contribute to the Economic Reform Roundtable and urge the federal government to consider the deep damage that scams and fraud inflict on financial wellness and productivity. Australia reported scam losses per capita were more than double those of the United Kingdom in 2024 and higher again in 2023.

Behind each statistic is a person, who commonly experiences shame, humiliation and long-term financial distress. Australian scam victims receive between 2 to 5% reimbursement, which increases marginally to 10% if victims complain to the Australian Financial Complaints Authority, where they undergo significantly elevated harm and are blamed for their scam.

Interpol, Amnesty and Operation Shamrock explain that transnational crime syndicates are behind the escalation in financial crime around the world. In 2023, scams took 0.11% of Australia’s GDP in reported losses. One UK fraud expert told our group “Australia is the number one fraud target in the world”, with professional scam compounds increasing the desks they devote to scamming Australians, who are considered trusting and wealthy by global standards.

Every scam - whether romance, investment, phishing, SMS or otherwise - depends on two key enablers:

1. The deception or impersonation of a trusted entity (or entities);

and

2. Money laundering to rinse the origin of scammed funds ‘clean’ to avoid being recovered by law enforcement or financial institutions.

None of this is in the national interest. Ignoring the epidemic of global scamming is not fiscally responsible in a cost-of-living crisis. Nor does it strengthen Australia’s budget sustainability. And with the rapidly increasing sophistication of Artificial Intelligence (AI), the situation will likely worsen without urgent legislation and regulatory changes.

Considering this, we offer the following recommendations for meaningful reform. Every Australian age group - from young to old – loses large amounts of money to scams. As a group with lived experience of navigating Australia’s broken system, we propose:

1. Government-led digital identity

Australia urgently needs a national digital identity framework that is resilient to fraud and impervious to criminal misuse. Public trust in government agencies and institutions is eroded when identities on banks, social media, email, the open web, telecom messages and calls can be impersonated with ease. Edelman’s 2025 Trust Barometer reveals Australians’ trust in governments and institutions is currently at an all-time low.

2. Create an economy-wide KYC Framework and better privacy

Know Your Customer (KYC) processes must be unified across banks, telcos, digital platforms, and financial service providers. Current fragmentation fuels risk and asks people to share their data across multiple platforms. Australia’s largest corporations have breached personal data - from Qantas to Medibank to Optus - and scammers wash the leaked data together to build profiles that are then targeted for scams and frauds.

3. Criminalise money laundering as integral to fraud-fighting

Fraud and money laundering are inseparable crimes. Stronger enforcement and clarity in law -mirroring reforms proposed under the AML/CTF regime - are essential to prevent stolen funds from flowing from Automatic Teller Machines into foreign currency, gold bars, crypto ATMs and other onshore and offshore ‘placement and layering’. State and federal law enforcement must have more power to use criminal justice laws. We also recommend increased transparency for scam victims to learn whether their stolen money is funding the crimes against humanity seen in overseas-based scam compounds.

4. Reform regulatory and law enforcement capacity

Australia’s current regulatory frameworks have failed to keep pace with cyber-enabled financial crime. Nationally harmonised laws - like the Australian Consumer Law - could empower agencies to act faster, more consistently, and at lower cost to taxpayers. We need to simplify the state-funded burdens these crimes are putting on our taxpayer-funded resources, which are currently inadequate and unsuccessful at delivering justice or restitution.

5. Require cybercrime insurance as a condition of housing incentives

The horrifying rise of real estate and home buyer scams, particularly through Business Email Compromise, demands immediate response. No financial institution offering federally subsidised housing loans should be allowed to operate without insuring consumers against cyber fraud. Many banks are profiting by charging interest on scammed losses and will have no incentive to change without government action.

6. Fund trauma-informed support for scam victims

The human cost of scams is not just financial. Dedicated mental health and trauma support services must be made available - beyond Medicare - to help victims recover and re-engage with the economy. We have many victims who can no longer function the way they once did. The scam is the first problem - it’s navigating justice (or the lack of it) and the devastating financial consequences that most victims report as debilitating.

7. Cut through the red tape nightmare to improve Scam Prevention Framework

While the proposed Scam Prevention Framework is a step in the right direction, in its current form it risks creating a bureaucratic nightmare - overburdening government agencies and traumatising victims, and clogging up courts with costly, time-consuming disputes.

Instead, the framework should be reworked to adopt key elements of the UK’s reimbursement model, which shifts responsibility onto the private sector - where the capacity and incentives to drive efficient, innovative solutions already exist. In the UK, this has reduced fraud by comparison to other wealthy scam-targeted countries. Mandatory reimbursement has not created the ‘honeypot’ that lobby groups have falsely claimed.

Rather than layering-on complex regulation that still forces justice on a case-by-case basis which is difficult and expensive to enforce, we need a smarter approach. We need banks, telcos and platforms to do better, not just the bare minimum. A well-designed “carrot and stick” model would encourage these industries to invest in fraud prevention and customer protection, rather than the current regime that encourages a race to the bottom with AFCA trying to pick up the pieces of each individual case.

Scams are a hidden productivity crisis

Scams are not just a consumer protection issue; they are an economic emergency. Scamwatch reported $2 billion in losses in 2024, with Consumer Action Law Centre saying 30% of victims do not report their losses. We believe the under-reporting is much higher. Scammed money could be better utilised to invest in homes, businesses, and community life.

As more Australians are defrauded, money is siphoned offshore, often into the hands of international crime syndicates. This weakens our tax base, limits our ability to fund services, and undermines long-term productivity.

The UK has acknowledged this. Its Attorney General recently argued that fighting fraud is essential “to kickstart economic growth.” Australia must do the same.

Addressing scams by improving identity systems, harmonising enforcement, and protecting victims will rebuild public trust and immediately enhance productivity. Every dollar that stays in our legitimate economy strengthens it.

Our submission speaks directly to the Roundtable’s goal of creating a more dynamic and resilient economy. We advocate that:

• Addressing scams is a prerequisite for sustainable economic growth.

• Plugging the holes that allow financial crime to thrive will preserve capital, restore confidence in institutions, and support households and businesses in a rapidly digitising economy.

• Strengthening identity systems, harmonising regulation, and enforcing accountability will make Australia safer for innovation, accelerate the adoption of trusted digital tools, and free up resources that can be invested in the net zero transformation, skills development, and more efficient service delivery.

For every dollar we protect from fraud, we gain productivity, trust, and the opportunity to invest in a stronger future. We are eager to engage further and share survivor-led insights that can shape a safer and more trustworthy financial system.

Thank you for considering our submission.

Sincerely,

Harriet Spring

President

Scam Victim Alliance